Synopsis: “A Brighter Future”, Episode 29

In this episode Richard Calhoun, CEO of Laidlaw Wealth Management, discusses the factors supporting the stock market both ahead of the November 2020 election and into 2021, the early takeaways from the Q3 2020 corporate earnings season, whether the Growth vs. Value investment style distinction has been disrupted, the question of whether investors should reduce stock market exposure going into the election and other developments with Laidlaw & Company Chief Market strategist, David Garrity.

The topics discussed in this episode are: What factors will support stock market appreciation after the November 2020 election?, Can corporate earnings growth in 2021 support a 3800 level on the S&P 500 index?, While investors consider rotating from Growth into Value, should we see this opportunity as just a trade, not a long-run investment shift?, and Should investors reduce stock market exposure in the run-up to the November 2020 election?

Please tune in for more timely insights.

Hashtags & Stock Symbols: #StockMarket #SP500 #Growth #Value #Disruption #Earnings #Fed #Economy #COVID $DIA $SPY $QQQ

SCRIPT:

Hello and welcome to another episode of “A Brighter Future,” Laidlaw & Co’s Podcast Series. I’m Rick Calhoun, CEO of Laidlaw Wealth Management, and once again I am joined by David Garrity, Chief Market Strategist for Laidlaw & Co.

David, I hope you had a nice weekend, caught some playoff baseball or college football and enjoyed the almost “picture perfect” weather here on the east coast.

Rick, it was a great weekend indeed with walks in the woods, kids diving into piles of leaves and pumpkins being carved, albeit with some modifications unique to 2020. Namely, as a nod to the current COVID pandemic, the pumpkins were given ears so they could wear N95 masks. While this may not serve to limit the spread of the Coronavirus, it nevertheless served to raise everyone’s spirits in anticipation of Halloween coming at the end of the month.

Question 1

David – last week we saw stocks oscillate between positive and negative territory, reflecting a tug-of-war between rising concerns and encouraging economic data. Weakness stemmed from a continued stalemate in stimulus talks, along with the recent rise in COVID-19 cases and the accompanying worries over implications for the continued reopening of the economy. Markets did find a lift from a positive U.S. retail sales report that showed consumer spending rose strongly in September despite the lack of renewed aid from Washington, signaling some resiliency to the recovery.

So, while I know we both believe that the broader fundamental outlook remains intact, is it fair to say that policy support, the path of the virus and the discovery of an effective vaccine, will be key drivers in the months ahead, after we pass the election, of course?

Rick, we have previously discussed “The Four Horsemen of The Recovery” which we see as Stimulus, Economic Data, The Fed, and Vaccine. Before we discuss each driver, it may be helpful to quickly check on stock market performance so far in 2020:

| Growth vs. Value: 2020 Performance By Quarter | |||||

| 1Q20 | 2Q20 | 3Q20 | 4Q to date | YTD | |

| Index | Change % | Change % | Change % | Change % | Change % |

| S&P 500 | -20.0% | 20.0% | 8.5% | 3.6% | 7.8% |

| S&P 500 Growth | -14.8% | 25.7% | 11.4% | 3.7% | 23.7% |

| S&P 500 Value | -26.0% | 12.4% | 3.9% | 3.7% | -10.3% |

| Growth less Value | 11.2% | 13.3% | 7.5% | -0.1% | 34.1% |

| Russell 1000 (R1K) | -20.6% | 21.2% | 9.0% | 4.0% | 9.1% |

| R1K Growth | -14.4% | 27.4% | 13.0% | 3.7% | 27.9% |

| R1K Value | -27.3% | 13.6% | 4.9% | 4.3% | -9.7% |

| Growth less Value | 13.0% | 13.9% | 8.1% | -0.5% | 37.6% |

| Russell 2000 (R2K) | -30.9% | 25.0% | 4.6% | 8.4% | -2.1% |

| R2K Growth | -26.2% | 30.8% | 7.1% | 8.0% | 11.7% |

| R2K Value | -36.2% | 18.8% | 1.9% | 8.9% | -15.9% |

| Growth less Value | 10.0% | 12.0% | 5.2% | -0.8% | 27.6% |

Clearly, Growth has massively outperformed Value over the course of the year as investors flocked to companies benefitting from the overall transition to “work from home” and the impact of social distancing on leisure and entertainment activities. For example, Gartner reported worldwide 3Q 2020 PC shipments were up +11.4% – the strongest growth in a decade. Google Chromebook sales (not included in the PC data) were up an astounding +90%. NPD data to August shows +23% growth for 2020YTD video game sales versus last year. Also, App Annie reported that hours spent on mobile apps around the world were up +25% percent for Q3 2020 year/year.

Still, we can see in the stock market that Value has been doing better so far in October as the market anticipates an improved economy in 2021. One question we will come back to in our conversation is whether it is time for investors to rotate to Value from Growth.

Now to handicap the ponies, Stimulus has become the football in the political brinksmanship ahead of the November 2020 general election. While there is constant news of negotiations between Congress and The White House, we are reminded of the line from Shakespeare’s “Hamlet” namely, “Words, words, words” which is to say that nothing will happen until after the election with the benefit to come in 2021. The prospects of a Democratic “Blue Wave” election outcome will bring with it the likelihood of a greater fiscal stimulus program, perhaps on the order of $5 trillion with the partial offset being higher income and capital gains tax rates. A mixed election outcome that leaves the Senate in GOP hands will probably be negative for the stock market as the amount of additional fiscal stimulus will be less.

Relative to Economic Data, the news has become mixed since the end of the supplemental unemployment assistance at the end of July 2020. Last week saw an uptick in the weekly unemployment data with an unexpected increase of +53,000 new claims on a seasonally adjusted basis (+76,670 not seasonally adjusted). There have been other weekly increases since May 2020, such as July 18th (+114,000) or August 15th (+113,000), so this is not all that unusual. Still, seeing this widely watched measure of labor market conditions moving in the wrong direction prompts closer inspection. One should understand that weekly unemployment data reports have been degraded for the following reason: national data has not included fresh unemployment insurance claim numbers for California for almost a month now.

Every week since September 19th, California’s initial claims have been 226,179, essentially unchanged from the May 9th level of 212,667. This reflects work by the California Employment Development Department to develop more robust systems, an effort that has caused a multi-week delay in processing new claims. Since California has 29% of all unemployed Americans receiving unemployment insurance, we have not been getting the full picture for the past month.

Meanwhile, other high-frequency economic indicators such as the NY Federal Reserve’s Weekly Economic Index (WEI) continue to show generally steady improvement in the US economy. The WEI uses a set of high frequency indicators to evaluate American economic output in almost real-time. These include initial/ongoing claims for unemployment insurance, same-store retail sales, steel production, gasoline and electricity usage, and other data points. For the WEI, the weekly reading is for a -3.9% GDP decline versus the 13-week average of a -5.6% GPD decline.

Relative to The Fed, the indications remain that Chairman Powell is prepared to do what is necessary to continue to provide monetary support for the economy while continuing to reiterate The Fed’s position that further fiscal stimulus efforts are necessary and required for a sustainable economic recovery.

Relative to Vaccine, all indications are that multiple efforts remain underway, but last week did bring news that the FDA is holding firm on ensuring that necessary vaccine safety protocols are followed prior to remedies being released for wide-scale distribution. This may not necessarily have been met with approval from The White House given the promises made there that a vaccine would be developed before the November election.

For now, from yesterday’s “Meet the Press,” we are reminded by Dr. Michael Osterholm, director of the Center for Infectious Disease Research and Policy at the University of Minnesota, that with infections rising and compliance eroding, “the next 6 to 12 weeks are going to be the darkest of the entire pandemic.”

Bottom line, while the election will soon be passed with a greater stock market upside should a Democratic “Blue Wave” be the outcome, the economy is managing to hang in there despite the delay in passing further fiscal stimulus, the Fed is as supportive as ever and COVID still has no vaccine to stop it and the world is falling prey to pandemic fatigue. For the current stock market race, I will put my money on Vaccine to win, Stimulus to place and Economic Data to show.

Question 2

David, as we have talked about on past episodes of “A Brighter Future,” the longer-term outlook for stocks is positive with support from

economic growth, corporate earnings and interest rates.

However, in reading the research reports that I have it appears most don’t believe the gains experienced since March will be matched in the

months ahead, but instead a new bull market could emerge due to an earnings uptick in the latter part of 2020 and then rebound strongly in 2021.

I know you increased our Year End 2020 S&P Target to 3800 which represents an increase of +9% from current levels, excluding dividends but how do we get there?

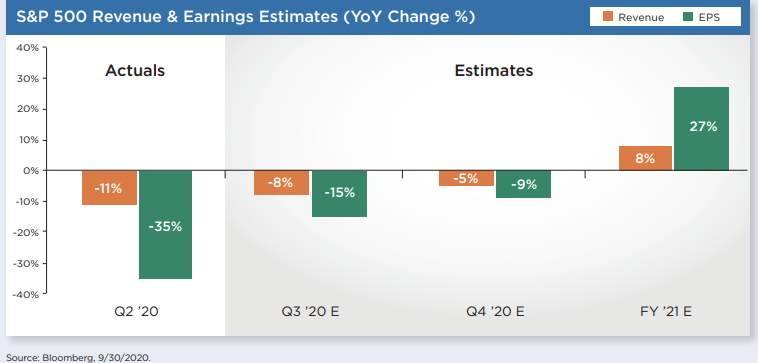

Also, do you agree with the recent Bloomberg report that said EPS could be up +27% for the FY2021?

Rick, we mentioned previously it is company profits that will drive the S&P 500 index higher. At start of September we said the 3Q 2020 earnings season would bring a repeat of the solid performance seen in 2Q 2020 when 83% of S&P 500 index companies beat EPS estimates (average outperformance +22.4%, a record) and 64% beat revenue estimates (average outperformance +1.6%). With the start of 3Q 2020 earnings season last week, we have not been disappointed.

So far, some 10% of S&P 500 companies have reported earnings, outperforming expectations by a substantial margin as 86% have surpassed Wall Street earnings (note the 5-year average is 73%). The average amount of the earnings beats is +21.7% over forecast on only a +3.6% beat on revenues.

This is the classic relationship between revenues and bottom line results of an early-cycle earnings recovery. Revenues only beat modestly, but profits are coming in much better as companies have cut costs so dramatically.

In sum, these better-than-expected results have begun to reduce the -21.2% earnings comparison analysts had in their Q3 models at the end of September. As of Friday 10/16, this comparison had narrowed to -18.4% versus Q3 2019. As such, Q2 2020 was the trough at a -32.0% comparison, so we are clearly past the corporate profits trough. Also, Wall Street analysts’ aggregate Q3 2020 EPS estimate for the S&P 500 is now $34.10/share, up +3.5% from September’s end. Estimates for Q4 2020 are rising as well, up +1.1% to $36.49/share.

Bottom line, Q3 2020’s annualized earnings run rate (4 x $34/share, or $136/share) is now back to 2017’s S&P 500 EPS level ($133.50). This is an impressive recovery in earnings power over a very short period of time. While it would be very welcome to have another fiscal stimulus package soon, Q3 2020’s reasonable earnings rate shows why markets feel they can wait if they must. This is not 2009, when S&P 500 earnings were coming off zero in Q4 2008.

All told, the corporate earnings performance we are seeing so far gives us sufficient confidence to reiterate our S&P 500 index price target of 3800.

Question 3

David, there has long been a discussion of “Growth vs. Value” but you recently made a great point that the better discussion might be “Disruptor vs. Disrupted.” Can you share with our listeners our conversation from this weekend, I think it’s a great topic with some very insightful observations?

Rick, last week brought the news that highly-regarded value-focused investment firm AJO Partners was closing down and returning capital to investors. To explain the decision, founder Ted Aronson said, “The drought in value — the longest on record — is at the heart of our challenge, we still believe there is a future for value investing; sadly, the future is unlikely to arrive fast enough — for us.” So, if Value investors are closing up shop, what is the flaw in the Growth vs. Value investment style discussion?

Our view is that the ranks of Value stocks are populated with companies whose business models are being disrupted. To that end, the classification should be not Growth vs. Value, but Disruptor vs. Disrupted. When the economy reaches a point where marginal gains start accruing to the Disrupted, then Value will rally. This is a more accurate characterization of the upcoming turn.

Along with the Disruptor vs. Disrupted distinction as superior to the Growth vs. Value classification, we should note the possibility that dividend payouts from Value names are likely to enter secular decline as the Disrupted need to reallocate capital towards self-disruption, much like Disney ($DIS) cutting its workforce and putting funds towards growing its streaming service or like IBM ($IBM) splitting off its growth operations (e.g. AI, cloud and quantum computing). If Value stock dividend streams decline, it undermines their appeal from a total return perspective.

As investors know, the basic equity valuation model is P = DIV / (r – g). If g < 0, then the effective discount rate increases. If that’s a secular phenomenon, then the case for Value stocks suffers as total returns come under pressure. Under this scenario we might say, Value: while not a feasible long-term investment approach, it can be a good trade.

Meanwhile, given the disparate impact of COVID on economies across the globe, whatever normal we return to, it will be one in which the world has been re-ordered. To our view, there is unlikely to be a return to what we had before. While there is an overwhelming tendency over time for reversion to the mean, the question we should address is what exactly will that mean be.

For now, the experience has been that Value outperforms early in the economic cycle when operating leverage rates are highly positive and driving in an accelerated manner operating cash flow levels higher, something underpinning the positive stock market performance of Industrial stocks now. This amounts to a cyclical trading opportunity, but not a long-run core portfolio holding.

In my view, this is reminiscent of the old Wendy’s commercial but the copy has been changed to: “Value: come for the sizzle, but where’s the beef?”

Question 4

David, as we bring this episode of “A Brighter Future” to a close with two weeks until the 2020 Election, I want look at its impact on the markets. Investing during an election cycle can be challenging on the nerves and 2020 promises to be no different. As we enter the final days before Election Day, news headlines on topics such as the presidential debates, campaign rallies, and a candidate’s COVID-19 test can draw strong emotions among investors and potentially move markets.

Historically, elections have impacted the market when they were imminent, especially in the final two to four weeks. Equity market volatility, represented by the VIX Index, has been slightly elevated in the month before an election on average and has been as much as +20% higher than the long-term average during the final two weeks prior to Election Day, the time we are in right now. So, what should people do? Do you sell now and lock in your gains at Lower Capital Gains rates since Biden says he will raise taxes and the polls says Biden is going to win. Do you “stay the course” as the market will probably “rip higher” no matter who wins since each side (Republican or Democrat) will implement more stimulus?

Rick, the lesson from history is that Presidential elections are no reason for investors to take their money out of the stock market.

Let’s assume an investor with $10,000 were to decide to wait out the first 100 days of each administration, what would be the difference between this investment strategy versus one where the investor remained fully invested in the S&P 500 index? The results show that staying fully invested allows the investor to realize 1.8x greater returns. In an analysis covering a period from 1957 to the present, the $10,000 grows to $790,000 if fully invested, only $426,000 if not, a 1.85x better result. In a shorter time-frame analysis covering from 1980 to the present, the $10,000 grows to $324,000 if fully invested, but only $169,000 if not, a 1.92x better result.

Other analyses looking at stock market performance over U.S. Presidential elections show the S&P 500 has generated an average price return of +0.9% with 60% positive in the one month prior to election day since 1945 (excluding recessions), with a high of +5.1% and a low of -2.3%. The price return in the one month following election day has been +1.3% on average with 60% positive since 1945 (excluding recessions), with a high of +5.8% and a low of -6.2%.

Bottom line, we believe investors are best served to remain exposed to equities through the upcoming November 2020 election in order to realize superior long-run returns.

Comments are closed.