In this episode Richard Calhoun, CEO of Laidlaw Wealth Management, does a mid-year tune-up of the December 2019 “Laidlaw 5” 2020 investment outlook and discusses positioning for 2H2020 and 2021 with Laidlaw & Company Chief Market strategist, David Garrity.

The topics discussed in this episode are: Growth dominated 1H2020 and will climb further until COVID contained, 2020 S&P 500 target 3,420, Election 2020 prospects favor Biden, Global GDP to contract -4.9% in 2020, Asset allocation still favors equities, and “Is Tech all an investor really needs?”.

Please tune in for more timely insights.

SCRIPT:

Hello and Welcome to a special episode of “A Brighter Future” Laidlaw & Co’s Podcast Series. I’m Rick Calhoun CEO of Laidlaw Wealth Management and I am fortunate again to be joined by David Garrity, Chief Market Strategist for Laidlaw & Co.

David, I hope you had a fantastic 4th of July holiday and enjoyable vacation.

As I said, today’s episode is a special one as we will do a Mid-Year Checkup on our “Laidlaw 5” Predictions as well as look ahead to what we think the rest of 2020 could look like.

Question One:

David, before we get into “Laidlaw 5,” it’s hard to believe that we’ve reached the halfway mark in 2020. If you’d glanced at the stock market on January 1st and then not again until June 30th, you’d see it was down a modest -4%.

But, as we are all well aware, that doesn’t even begin to tell the story of the first six months of this year. The first half of 2020 contained an all-time high for stocks, a global pandemic, the deepest recession since the 1930s and the sharpest bear market drop on record, followed by a market rally that included the fifth-strongest quarterly gain in the postwar era. So, with all of that packed into the first half of the year, what do you do for an encore?

Rick, it would indeed be fortunate if after all that has transpired so far in 2020 we could just declare victory and go home, but clearly the fight against Covid-19 (“COVID”) is far from over in terms of containment, first, and development and commercialization of a vaccine, second.

As we can see, the COVID containment struggle is setting up to be protracted effort as moves to re-open local economies without implementing adequate testing, tracing, social distancing practices and healthsystem capacity have shown without fail a relapse to rising infection rates. So, patience and persistence are the watchwords as impatience only serves to unmask the danger COVID presents.

With that, the prospects for further stock market gains from here depend primarily on what further fiscal programs governments around the world can provide to support economic activity while the top priority of COVID containment is pursued. In this regard, note with interest J.P. Morgan Chase comments that global debt issuance in 2020 will rise $16 trillion to bring combined private and public sector issuance to a record of more than $200 trillion with the main implication being that this will be positive for equity markets as most of the additional liquidity is expected to find its way into stocks.

As a fine example of government-directed asset inflation, note that China’s CSI 300 Index has now added +14% in five days, the most since December 2014, following influential state media pushing for a “healthy” bull market, a move most likely followed by state-controlled funds helping to drive prices higher.

Bottom line, with near-term private sector earnings prospects uncertain as 80% of the S&P 500 index members have withdrawn guidance, government fiscal programs will continue to be the source of liquidity needed to power the equity market flywheel. With the November 2020 U.S. general election coming up fast, we expect another program on the order of the $3 trillion passed in March 2020, this should provide a level adequate to keep the S&P 500 index moving steadily higher towards our “Laidlaw 5” 2020 target of 3,420, up +9% from the Thursday July 2nd close.

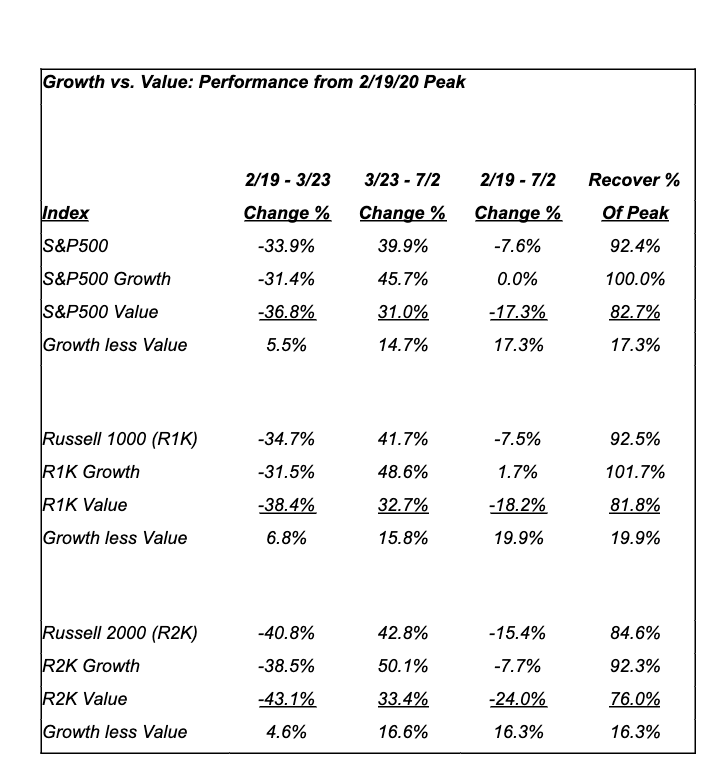

In looking for the next move, good to check stock market performance since 2/19/20.

Clearly, Growth is massively outperforming Value across the various market cap categories as investors remain uncertain about the prospects for economic recovery with COVID outbreaks recurring around the world. With Growth being seen as offering clearer prospects, it has become the “go-to” choice for investors and in the process more than recovered its February 2020 level. For Value to outperform, COVID containment must be achieved so as to provide greater certainty the economic recovery will be uninterrupted.

Question Two:

David, as I mentioned at the outset, today’s episode will be a “Check Up” on our “Laidlaw 5” 2020 Outlook. So, let’s get into it and tackle one of the traditional “third rail” topics, Politics. At the time we rolled out the “Laidlaw 5” in December 2019 it was a very different world and we thought the U.S. Presidential contest could be between Donald Trump (GOP) and Michael Bloomberg (Democratic), but we also talked about the potential of a “brokered” convention. Six (6) months and a Black Swan, Pandemic later things look a little different. History shows us that elections tend to be short-term catalysts for volatility as opposed to a long-term determinant of market performance, but the polarized political environment seems likely to prompt episodes of market indigestion as we progress toward November. The market appears rather complacent on the election uncertainties for now, so what are your thoughts as people start to focus more on November?

Rick, Not wishing to strike only one note here, but it appears that the November 2020 election will follow the COVID tune. To this end, we see Trump’s approval rate is slipping fastest in the 500 counties in the U.S. where COVID deaths have exceeded 28 per 100,000 people, according to Pew Research polls. Older voters who typically trend conservative are abandoning him.

As COVID’s persistence is prompting firms such as Goldman Sachs to cut economic growth forecasts lower (i.e. 2020: -4.2% to -4.6%), the prospects for GOP re-election may likely hang on moves such as limiting “vote-by-mail” since they are unable to run on a record of strong, sustainable economic growth thanks to COVID.

On this point, while the June employment report was a pleasant surprise with a gain of +4.8 million jobs, the spread of COVID in the South and West has served to dampen the rise in foot traffic following local moves to reopen the economy. COVID outbreaks represent a well-defined speed bump for the U.S. economy on its road trip to recovery. With the $600 weekly unemployment supplement scheduled to end on July 25th, COVID outbreaks suppressing consumer activity comes at a very bad time for the +20% of the population that relies on consumer discretionary spending to employ them and pay their wages. There are still 31 million under- and unemployed Americans, so in an election year more fiscal stimulus is certain, but whether it will be sufficient to prevent massive GOP losses in November is unclear.

Meanwhile, despite the announcement over the July 4th weekend via Twitter of the dark-horse Presidential candidacy of Kanye West, the 2020 Presidential race is between the incumbent Donald Trump and former Democratic Vice President Joe Biden. While Biden has a history of making unfortunate gaffes while coping with a life-long stuttering issue, his legislative and policy experience along with his moderate position within the Democratic Party should serve to pave his way to The White House in the November election.

Kanye West notwithstanding, the surprise development we may see is an August 2020 announcement by Donald Trump that he will not accept the GOP nomination and withdraw from the 2020 Presidential race. Over the past two years the president’s re-election effort has raised more than $947 million, and has about $295 million cash on hand. Being President has been remunerative for Trump Inc. Assuming a deal can be struck to limit prosecution for Trump once he leaves office, a withdrawal decision is likely assuming that COVID containment efforts continue to fall short and poll results deteriorate concomitantly.

Question Three:

The next topic from the “Laidlaw 5” was the Macro-Economy. At the time, we felt the global macro-economy was likely subdued as major events such as the U.S.-China trade tariff confrontation and the distinct possibility of a hard “Brexit” by the U.K. from the E.U. remain unresolved. We also thought there was the possibility of an exogenous shock, with an increase in oil prices to the $75/barrel, of course the exogenous shock was a virus from China. With this as back-drop, what are your thoughts on the Macro-Economy?

Rick, starting from the baseline of the IMF forecast calling for a -4.9% contraction in the global economy, the real forecasting question is what are the prospects for 1) rebound in 2H2020 and 2) real recovery in 2021.

While some gauges of manufacturing and retail sales in major economies are showing improvement, hopes for a V-shaped rebound have been shattered as the reopening of businesses looks shaky at best and job losses risk turning from temporary to permanent. Note that true recovery means you are at least as well off as you were before the crisis started and from all available data it is apparent that we are a long way off that thanks to COVID.

As such, COVID holds the upper hand not just in the U.S., but worldwide. The IMF estimates that by the end of 2020 170 countries, almost 90% of the world, will have lower per capita income. This marks a complete reversal from January 2020, when the IMF predicted 160 countries would have bigger economies and positive per capita income growth.

Bottom line, the prospects for 2H2020 rebound depend on sustained fiscal and monetary support along with successful COVID containment. Together, achieving these two milestones along with a COVID vaccine being developed would lay the foundation for recovery in 2021.

Question 4:

The next topic was a call, and a great one, on both Interest Rates and Staying Invested as we said with rates continuing to drop the idea of “TINA” or There Is No Alternative to the equities would become even more important. With the Fed signaling a Zero Interest Rate policy until 2022, how should investors be positioned?

Rick, while our discussion to this point underscores how the equity market is the primary beneficiary of the liquidity provided by fiscal relief programs, investors need to address first the asset allocation decision as that is the greater driver of long-run investment returns. We think equities should represent 50-55% of overall portfolios with an emphasis on Growth over Value until there are clear indications that COVID containment efforts are sustainably working at which point Value could be over-weighted.

Relative to fixed income, U.S. 10-year Treasury yields have tumbled by more than 100 basis points this year to around 0.67%. The prospect of negative interest rates, however undesirable to Fed Chairman Jerome Powell, offers some chance of further interest rate declines. Globally, monetary relief efforts will continue as the COVID crisis is far from over. Morgan Stanley predicts $13 trillion in cumulative central bank balance-sheet expansion from the U.S., euro region, Japan and U.K. through the end of 2021. Bottom line, our view is fixed income should receive a 35-40% allocation with yield-oriented investors looking to have corporate or high-yield issues represent 55-60% of the fixed income allocation.

The balance of the portfolio allocation of 5-15% should go into a mix of inflation hedges such as gold, commodities and real estate. We note that the longer interest rates are at a zero bound and the prospects for liquidity-driven inflation grow, gold looks to appreciate from current levels. For commodities, producers in the energy and metals sectors have brought in production levels sufficiently to allow prices to remain stable and possibly rise as economic growth resumes. For real estate, while COVID driving a distributed workforce model does not favor higher occupancy rates, low interest rates do allow for a higher present value for the portfolio of long-term lease agreements that real estate represents.

Question 5:

Finally, we talked about the potential of profit margins depressing for Alphabet and Facebook but due to greater regulation not a boycott by advertisers. Despite the problems Facebook is facing right now though, Tech is “on fire” During the first half of 2020, the Nasdaq 100 rallied almost +17%, sprinting past the S&P 500 index, which fell -4%. The numbers look even better for a broader basket of tech companies. Barron’s this weekend ran a report showing tech stocks with market values of more than $5 billion—a group of 200 —and found an average first-half return of nearly +26%!! So you do investors just need to “close their eyes” and buy a Tech ETF?

Rick, when it comes to how the Tech sector has been revalued during COVID, we need to appreciate that developments that were expected to take 10 years to unfold have been accelerated in as many weeks. As such growth has been brought forward. A review of how more time has been re-allocated to Tech-based activities serves to drive this point home.

Before COVID, Americans spent almost an hour commuting and a similar amount of time shopping every day. With “work-from-home” (WFH) still prevalent across the U.S., that amounts to almost 2 hours up for reallocation. The winners of this time-grab have been everything from social media to hardware suppliers to exercise platforms. As long as WFH persists these sorts of names will continue to take market capitalization from companies “losing time”.

That said, buying an ETF comprised of the companies that are “time takers” and shorting an ETF comprised of companies of “time losers” would be a sensible investment strategy as the trends unleashed by COVID appear to be sustainable.

Bonus Question:

What is one thing you think we could see in the second half of 2020 that no one else is focusing on?

Rick, I’m tempted to go with Kanye West becoming President of the United States as the wild card on this one. However, there is one development possibly occurring in China that could be quite a surprise, namely an earthquake-induced collapse of the Three Gorges Dam on the Yangtze River.

A major piece of infrastructure that when constructed in 2006 was the largest dam in the world, the Three Gorges Dam created an immense deepwater reservoir allowing ocean-going freighters to navigate 2,250 km (1,400 miles) inland from Shanghai on the East China Sea to the inland city of Chongqing.

Following steady rainfall in the Yangtze River basin over the past month, there have been within the past week earthquake-induced landslides upriver from the dam’s location. Note that the Three Gorges Dam sits on two major fault lines, the Jiuwanxi and Zigui-Badong, and that massive changes in water pressure in the dam’s reservoir due to flooding could lead to earthquakes, a phenomenon known as reservoir-induced seismicity, which in turn would lead to landslides that would at the very least exacerbate the flooding in the area and potentially threaten the integrity of the main dam.

A failure of The Three Gorges Dam would be a catastrophic tragedy that would most likely drive China further into recession as its ability to support global supply chains from the Yangtze Basin interior manufacturing base would be severely compromised.

That said, Rick, we remain for now a bull, albeit in a china shop.

Comments are closed.