Synopsis: “A Brighter Future”, Episode 25

In this episode Richard Calhoun, CEO of Laidlaw Wealth Management, discusses the 2020 Q3 outlook, the 2020 election season, Tech sector market leadership, the Fed and other developments with Laidlaw & Company Chief Market strategist, David Garrity.

The topics discussed in this episode are: What are final marks for 2020 Q2 earnings season and what now for 2020 Q3 earnings?, What portfolio moves should investors make ahead of the November 2020 election?, Is the Tech sector’s market leadership overdone?, What takeaways are there from Fed’s June 2020 minutes?, and Should silver be in the portfolio and what appreciation potential is there for the S&P 500 for the rest of 2020?

Please tune in for more timely insights.

SCRIPT:

Hello and welcome to another episode of “A Brighter Future,” Laidlaw & Co.’s Podcast Series. I’m Rick Calhoun, CEO of Laidlaw Wealth Management, and I am fortunate again to be joined by David Garrity, Chief Market Strategist for Laidlaw & Co.

David, I hope you had a nice weekend. Did you get a chance to do some more fishing with your sons?

Rick, last week we decided to test our fishing fortunes on the open sea. The younger members of the crew caught fluke and sea robin, both of which were enjoyed later for dinner. Me, I caught crabs, who just like the financial markets are showing a great tenacity and staying power.

Question 1

David, last week the S&P 500 edged past its pre-pandemic record high reached in February. It was a milestone that marked the roundtrip rally from lows to highs as the fastest bear-market plunge and the second-fastest bear-market recovery in U.S. history. In contrast, the economy has not had a chance to recover as swiftly from the plunge in economic activity in the second quarter as a result of the pandemic and the national and global lockdown measures to contain it.

The good news is that, after the greatest decline in economic activity since the Great Depression in the second quarter, the economy has shown signs of recovery. The bad news is that with COVID-19 cases still at elevated levels, the momentum of that rebound has softened in August.

So, with most of Earnings Season behind us and in the spirit of “Back To School,” what grade would you give the overall earnings results and what should we expect for the 3rd Quarter?

Rick, as you may recall the onset of the COVID-19 Coronavirus (“COVID”) pandemic prompted roughly 80% of the companies in the S&P 500 index suspend financial guidance. You know, in 2020 H1, analysts cut 2020 estimates for S&P 500 index companies by -28.7%, the largest decrease for any H1 since the data was collected starting back in 1996. At the same time, 2021 estimates were cut by -16.9%. With all this being the case, Wall Street was left in the position of preparing for the worst and hoping for the best.

So, with this kind of a setup, it was not a surprise that 2020 Q2 managed to blow past the massively decreased expectations as 83% of S&P 500 companies reported a positive EPS surprise (+22.4% ahead of forecast) and 64% have reported a positive revenue surprise (+1.6% ahead of forecast). This marks the highest percentage of S&P 500 companies reporting a positive EPS surprise since the data was tracked starting in 2008 and sends the clear message that to handle COVID companies are getting a clear fix on their operating costs so profit margins are much stronger than they were previously feared to be.

While some observers might claim that company managements were sand-bagging earnings guidance, I would differ and give credit where it is due in recognizing managements’ discipline in battening down the hatches to deal with the demand devastation from COVID. Separately, as discussed in earlier episodes, corporate profits have to now always followed a “V-shaped” path in recovery and 2020 Q2 results clearly serve to underscore to investors this critical point.

So, where does this leave us in terms of an encore? Off the back of Q2, estimates for both 2020 and 2021 are moving higher. Thus far in Q3, analysts have raised EPS forecasts for 2020 and 2021 by +3.5% and +1.4%, respectively. The path of the EPS and revenue recovery for the S&P 500 is shown in the table below:

| Forecast Expectations: S&P 500 | ||

| Period | Revenues | EPS |

| 2Q 2020 | -9.8% | -33.8% |

| 3Q 2020 | -4.4% | -22.9% |

| 4Q 2020 | -1.4% | -12.8% |

| 1Q 2021 | 3.1% | 12.9% |

| CY2020 | -3.2% | -19.0% |

| CY2021 | 8.4% | 26.5% |

Bottom line, we are encouraged by the strength of corporate performance relative to expectations and are of the opinion this will carry over into 2020 Q3 earnings season which will start in October, being nevertheless mindful of the COVID risks that persist.

Question 2

David, last week the election news cycle kicked into full gear with the Democratic National Convention (held virtually for the first time). This week, the Republican National Convention will take center stage. I am sure we can expect election news will dominate headlines through November, and election uncertainty may cause short-lived market volatility.

However, stocks have performed well in all types of political configurations, returning +10% on average over the past 100 years regardless of which party occupied the White House or controlled Congress. What matters more for investor portfolios over the long term are economic and corporate fundamentals that support the rise in stock prices over time.

So in light of that, David, is there an “Election Playbook?” For example, if Democrats win how should investors position portfolios vs. an outcome that favors Republicans?

Rick, as much as one might wish there were an “Election Playbook,” for 2020 the impact of COVID on the political economy does not have useful historical parallels. For 1918, it was a midterm election in the U.S. that was affected by the Spanish Flu epidemic. However, one should note that the Bolshevik Revolution in Tsarist Russia unfolded against the backdrop of the Spanish Flu epidemic. Not a political outcome one might want to see in the U.S. this year as revolutions tend be decidedly disruptive.

With the collapse of the global economy due to COVID, it is not surprising to see Trump’s re-election prospects under pressure.

The Republican National Convention kicks off today with the theme “Land Of Promise,” appropriate perhaps since one hopes better days lie ahead should COVID be contained to allow the economy to recover. Of note, as is typical for Trump, the nominee will break from conventional practice by speaking at 10:00pmET every night of the conference rather than restrain himself to one appearance to deliver the acceptance speech on the last night of the convention. The one major development that might change the narrative for Trump is the discovery and commercialization of a COVID vaccine, but on this score time is running short as the fatality count relentlessly rises.

Turning to the prospects for a “Blue Wave” in which the Democrats win both chambers of Congress, the odds as shown by PredictIt are favorable for a Democratic sweep although the odds have tightened over the past month.

Relative to investor positioning for a Democratic sweep, the greatest concern for equities will be an increase in the corporate tax rate to 28% from the 21% rate now that would mute the benefit from the “V-shaped” profit recovery path mentioned earlier. On a positive note, companies positioned to participate in clean-energy infrastructure should be of interest. There are ETFs for the sector (e.g. ICLN, $16.29, $1.2bn market cap, +38.6% for 2020 to date) that are enjoying gains in the run-up to the November election. Also, as new revenue sources are desirable, it is likely that cannabis legalization will spread under a Democratic administration. According to the Institute for Taxation and Economic Policy, there were over $1.9 billion in revenues in 2019 from excise tax and sales tax in states with legal recreational sales. Estimates are that national legalization could produce nearly $130 billion in additional tax revenues and over 1 million jobs nationwide. There are ETFs for the sector (e.g. MJ, $12.40, $542mm market cap, -27.6% for 2020 to date) that have underperformed the broader stock market.

Under a Trump second term with a divided Congress, we expect Defense stocks and Energy stocks should prove attractive in part reflecting an aggressive “America First” foreign policy in addition to regulatory roll-backs.

Question 3

David, one of the other big market stories from last week was Apple becoming the first company to have a $2 trillion dollar market cap, extending a historical run that’s lasted decades.

Yet a statistic I heard caught my attention: It took AAPL 39 years (from the IPO in 1980 till October 11, 2019) to achieve a $1 trillion market cap. It took AAPL stock less than a year to go from a $1 trillion market cap to a $2 trillion market cap and that doubling of market cap occurred during the worst pandemic in 100 years.

Obviously, the surge in AAPL stock price isn’t fundamentally based, the company is doing well, but not that well. Much of that gain has been fueled by liquidity, i.e. investors piling cash into companies that they believe are immune from the negative effects of the coronavirus. Said differently, part of the increase in AAPL market cap is being driven simply by liquidity/asset inflation. The world is awash in liquidity, and investors, both retail and institutional are taking that liquidity/ cash and piling it into assets such as real estate, bonds, and stocks, especially secular growth stocks such as AAPL, AMZN, FB, GOOGL, MSFT, etc.

I think most investors are happy AAPL is a $2 trillion company, as almost everyone invested has exposure to AAPL somehow through index funds or mutual funds and they make fantastic consumer electronics. But, let’s not confuse the explosion in AAPL shares and other tech giants with similar explosions in revenue or profits. A lot of the gains in 2020 are driven solely by the anticipation of continued and accelerating asset inflation. What does that mean for our listeners? Is this something we should be concerned about?

Rick, put succinctly, COVID has provided the Tech sector a window to pursue disruption on steroids. As we have discussed in earlier episodes, COVID in substantially disrupting the global economy has brought forward in time growth opportunities for tech stocks such as Apple.

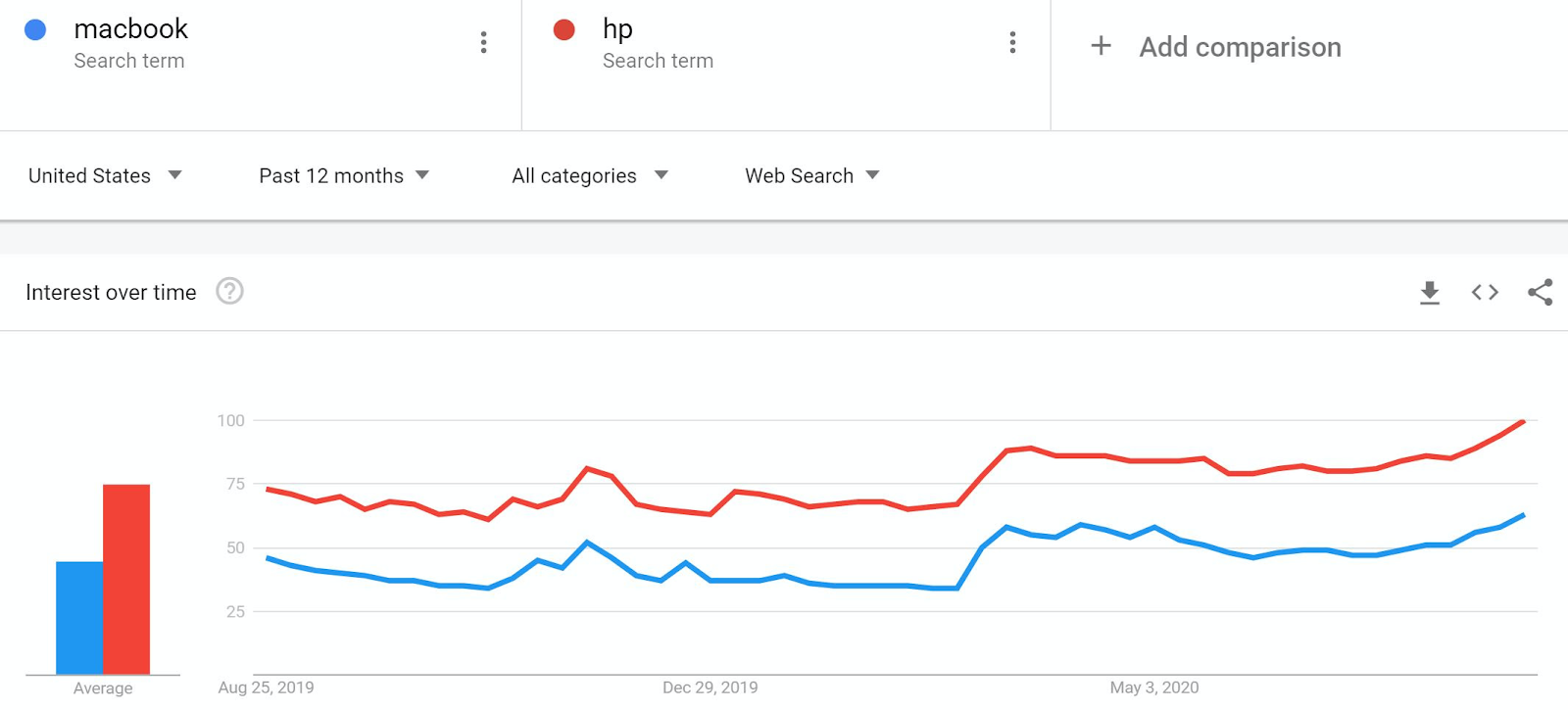

For example, Electronics continue to benefit from the pandemic, especially as Americans prepare for the new school year. Most schools and colleges are incorporating some virtual learning. As we can readily see both may get shut down again depending on the virus case count this fall. Google searches for “Macbook” and “HP” continue to climb and are higher than even November 2019 when queries typically spike around Black Friday. On top of that, they are even higher than the levels around the initial COVID outbreak and national lockdowns in April. If you’re wondering why Apple is a $2 trillion market cap company, this graph goes a long way to explaining that remarkable number.

While one could say that the current demand is not sustainable, bear in mind that as a result of COVID consumers and businesses have become more reliant on technology products and services. In terms of how individuals’ time is spent the shift to “work from home” has resulted in two hours being reallocated as activities such as physically commuting have been lessened. The longer COVID persists, the more these changes in behavior will become engrained. In comparison the “Internet 1.0” and “Y2K” Tech bubble were not founded on sustainable changes in consumer and business behavior. In the case of COVID the shift is founded on new behaviors that are becoming increasingly engrained as society shifts to a new standard.

That said, we are mindful that fiscal and monetary relief to offset COVID will diminish over time, perhaps sooner should Congress fail to act prior to the November election. Diminished liquidity inflows would serve to brake the flywheel that elevated share prices. This is not a market to chase aggressively, but still one to participate in as we expect the averages will grind higher into the end of the year.

Question 4

David, it seems like just about every day there is some discussion about the Fed yet typically FOMC minutes are a non-event for the markets, but that was not the case this past Wednesday as the markets interpreted the minutes as “not dovish enough,” and that caused a decline in stock prices and a rally in the dollar and the 10-year Treasury yield (a typically hawkish move).

So, what did we miss? I did not read anything in the minutes that appeared hawkish. Is this a case of the market assigning dovish expectations to the Fed and if their future comments are “max dovish” it will be a disappointment?

Rick, I believe the market was disappointed that in the June 2020 Fed minutes there was no indication of an immediate response to the signs of economic recovery weakening, that the Fed was possibly holding off on making a September 2020 shift to yield curve targeting. This response shifted the burden of market expectations over to the fiscal relief efforts in which Congress appears to be stalled over issues such as relief aid for state and local governments and additional funding for the U.S. Postal Service to support “mail-in” balloting for the November election.

I would say that investors may have been too quick to judge the Fed as this week will bring the Kansas City Federal Reserve Branch’s economic symposium scheduled for August 27th to 28th which is normally held in Jackson Hole, WY but will instead be held virtually this year. Fed Chairman Jay Powell will have a presentation on Thursday that may prove interesting in terms of previewing the changes the Fed is making in terms of inflation targetting, so stay tuned.

Question 5

David, as we bring today’s episode to a close, I thought it would make sense for us to discuss our Investment Committee meeting from the past week, specifically the decision to implement a position in Silver. As well, give the opportunity to discuss our new 2020 S&P 500 price target and the evidence supporting the decision for the change.

Rick, we have discussed before the weakness of the U.S. Dollar to other currencies as the pace of recovery domestically has lagged other economies. As then noted, it is a normal pattern seen in previous economic cycles. In such a scenario, alternative U.S. Dollar-denominated commodity investments such Gold and Silver have performed well with Silver outperforming Gold by 55% as shown in the table below.

| Historical Performance: Gold and Silver | |||

| Silver/ | |||

| Period | Gold | Silver | Gold |

| 1976-1980 | 717% | 1063% | 1.48 |

| 1985-1987 | 75% | 97% | 1.29 |

| 1992-1996 | 25% | 58% | 2.32 |

| 2001-2008 | 289% | 383% | 1.33 |

| 2008-2011 | 164% | 367% | 2.24 |

| Average | 254% | 394% | 1.55 |

With this in mind the Laidlaw Wealth Management Investment Committee has added a position in Silver to that of Gold which has been in the model portfolio since 2019.

Relative to the price target for the S&P 500 index, when the “Laidlaw 5” was published in December 2019, the 2020 S&P 500 price target was set at 3420, a level now +0.7% above last Friday’s close. We are increasing the 2020 S&P 500 price target to 3800, a level indicating +11.9% appreciation potential, based on the following considerations.

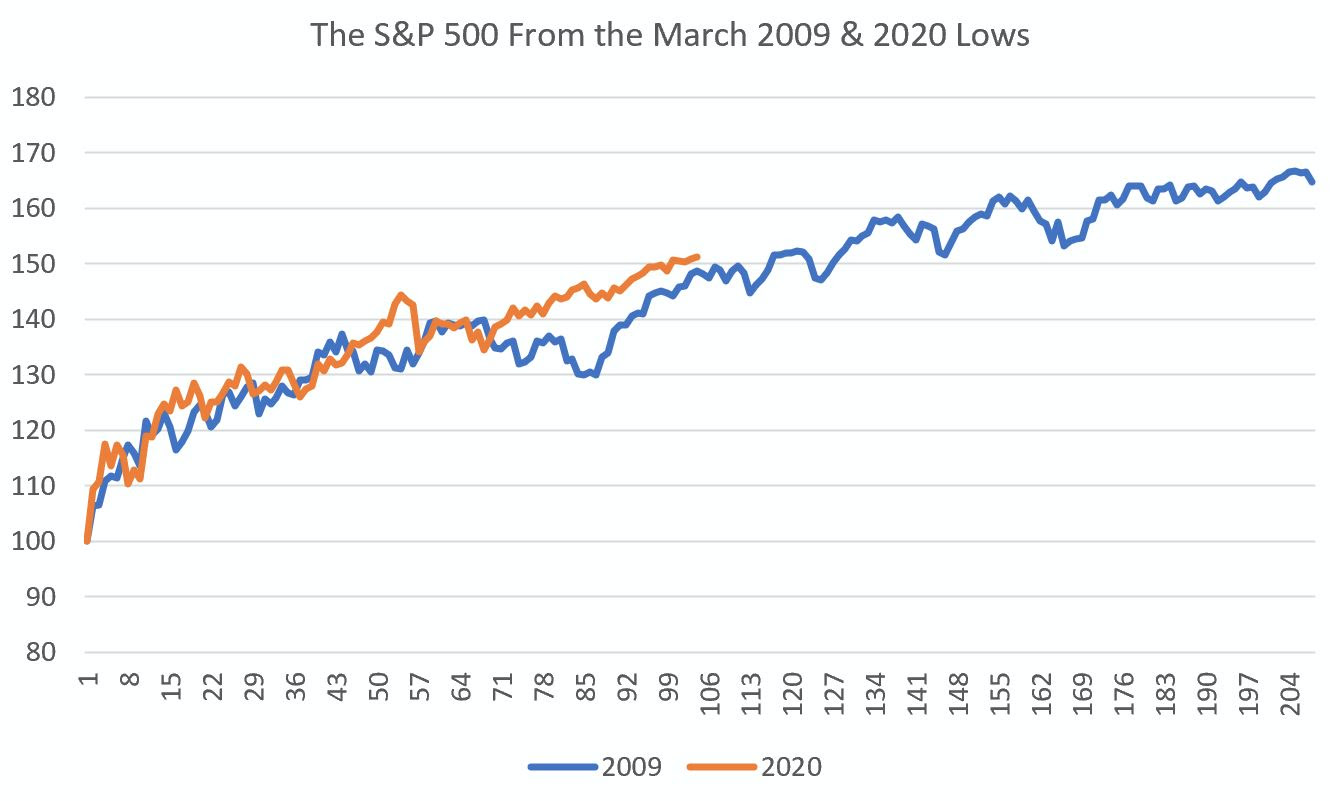

First, the current stock market recovery is tracking closely to the arc of the recovery seen in 2009.

The match is quite close, and 105 days from the 2009/2020 lows the S&P is just slightly better (+2 percentage points) than back in 2009 on the same trading day. That the 2009 experience points to a further gain between now and the end of the year is welcome news.

3 further thoughts on this comparison, both for good and bad –

1) The leadership groups in the 2009 rally were much different than in 2020. In 2009, the Financials doubled from March 9th 2009 to this point in the rally. That move gave investors a valuable signal that perhaps the Financial Crisis was over and that equities were safe to buy again. The narrative in 2020 could not be more different. Big Tech is leadership as it gains consumer and business share of wallet and attention. More on this below.

2) 2009’s rally occurred after a US Presidential election, where 2020’s move is happening just ahead of one. In many ways 2009 was such a good year (+26% for the S&P 500) because 2008 had been so bad (-37%). One reason 2008 was so horrible was the delay in providing fiscal stimulus (ARRA) until February 2009. Lawmakers barely passed TARP in 2008, and with the November 2008 election and change in power there was no consensus about fiscal stimulus until a new President and Congress took office in early 2009. This time around, the S&P 500 is heading into election season at essentially full throttle. Fair enough – it’s logical enough to believe that no matter which party wins White House and Congress there will be further fiscal stimulus. Most importantly, this is clearly different from 2009.

3) The belief in a powerful rebound in corporate earnings is the most important similarity between 2009 and 2020. During the Financial Crisis, S&P 500 annualized earnings went from a trough of $43/share (in Q1 2009) to $57/share at the end of 2009 to $91/share in mid 2011, a new record high. This time around, S&P earnings are troughing at $117/share (in Q3 2020) but analysts expect they will be at fresh record highs ($163/share) by the end of next year.

In summary, the comparison of 2009 and 2020 is ultimately a reminder that A) bottoms occur when government policy responses match the scope of an economic downturn and B) the nature of the market’s recovery will vary by sector, but the aggregate return (driven by a sharp earnings rebound) is closer than one would think likely.

So, how does the S&P get to 3,800 as this is the indication of where the 2009 playbook says it should go by year end? Consider the following:

1) Forget about cyclical rotation driving stocks higher if that means Tech + Google, Amazon and Facebook falter along the way. These stocks are collectively 38% of the S&P 500. Financials and Industrials (together 17.8% of the index) could rally +10%, but if that meant a -5% pullback for Big Tech then the S&P 500 would remain unchanged.

2) We need to see earnings estimates for 2021 continue to rise. An S&P 500 rallying with a 22x multiple means just one thing: investors think 2021 earnings are going to be better than expected. The latest FactSet data (chart below) shows this is happening, but it has to continue. That means a steady drip of better than expected economic data is needed critically.

3) Whatever happens with the November 2020 elections needs to be decisive. Remember the lesson of 2008 from 1) supra: political dead zones hurt stocks if the US economy is on shaky ground.

Bottom line, we remain positive on US equities, but recognize fully the next +10% move for the S&P 500 will likely be a more difficult climb than the last +50%.

Comments are closed.