Hello and Welcome to another episode of “A Brighter Future” Laidlaw & Co’s Podcast Series. I’m Rick Calhoun CEO of Laidlaw Wealth Management and I am fortunate again to be joined by David Garrity, Chief Market Strategist for Laidlaw & Co.

Good Morning David. I hope you had nice weekend and were able to get outside, soak up some sun and enjoy the beautiful weather while of course social distancing ? …

Yes, Rick, it was a great weekend. The one thing I did get close to was my grill.

David, we had another interesting week with over 160 of the S&P 500 companies reporting their 1Q20 Earnings among them every-day names like APPL, AMZN, MSFT just to name a few and at the same time we got some not so great economic indicators chief among them another staggering first time Unemployment Claims Report putting the number of people filing for a first time unemployment at almost 30 million!! The markets seemed to follow the news flow this week as S&P 500 gained +3.6% during the first three days of the week, only to give it back dropping -3.7% on Thursday and Friday. While the Dow and NASDAQ were both essentially flat for the week also following a similar pattern.

In looking at the current environment and with so many public companies suspending guidance, does the old Wall Street adage “Sell in May and go away” appear like it could make a return in 2020?

Rick,

While the weekend weather definitely made a seasonal turn for the better with clear skies and sunshine, the market ended last week on a decidedly clouded note as major companies such as Amazon and Apple either indicated that their 2Q20 profits would be eliminated by the costs of protecting their workforce and customers from the COVID-19 Coronavirus (“COVID”) or were sufficiently uncertain on the outlook for their product and service sales as to suspend even offering near-term earnings guidance.

Looking at 1Q20 corporate earnings season more broadly, with 55% of the S&P 500 having reported financial results, earnings are down -13.7% from 1Q19. This comparison includes both companies that have reported and what analysts have in their models for those yet to release results. The prospects are that corporate profits will fall more sharply year-over-year in the quarters ahead as Street earnings estimates are looking for more of a “U-shaped” profits recovery than a “V-shaped” snap-back:

1Q20: -13.7% on +0.7% revenues

2Q20: -36.7% on -9.5% revenues

3Q20: -21.0% on -4.3% revenues

4Q20: -9.4% on -0.5% revenues

Looking out further, for the S&P500 the Street has $134/share for 2020 and has not adjusted 2021 with estimates at $168/share (+25% growth). On a more conservative view of $147/share (+10% growth), the S&P 500 is trading at 19x earnings, not exactly cheap.

To your question of “sell in May and go away,” I would say that apart from the prospect of accelerating profit declines to contend with, there is another market pattern for investors to address, namely “The Fed Drift.” That is the well-documented phenomenon where the S&P 500 rallies from the open of a Fed meeting through the day after its conclusion. The Fed’s own work on the topic shows that from September 1994 to March 2011 (+17 years) the entire move in the S&P500 occurred in the 3 days around Fed meetings, most specifically Fed meetings where an updated Staff Economic Projection (SEP) was offered.

While last week saw a nice bump around the Federal Open Market Committee (FOMC) meeting on 4/28-29/20, the next Fed meeting is set for 6/8-9/20.

With 1Q20 corporate results winding down and the Fed on the sidelines for May, the main factors investors have to focus on now are: 1) the pace of economic decline (here, the NY Fed’s “Nowcast” model puts 2Q20 GDP at -9.3% following on 1Q20’s -4.8% GDP decline), 2) an increasingly fractious political environment in Congress likely to result in delays in further fiscal assistance being moved forward, 3) the uneven pace of the global economy coming off the first round of COVID lockdown, and 4) news of advances in developing possible COVID tests and vaccines. In short, a mixed bag. That said, a little more prudence and selectivity may be in order for investors in today’s market.

This week’s big event is the April employment report due out 0830ET Friday 5/8. While the survey period end was three weeks prior, we can get a more real-time read on employment conditions with the U.S. Daily Treasury Statement’s (DTS) data on “Withheld Income and Employment Taxes.” The 4/30/20 DTS shows Treasury receiving $182.6bn in “Withheld Income and Employment Taxes,” an amount -14.6% down from April 2019. Look for the week to end on a down note if the employment data comes in with a year-over-year decline worse than DTS report indicates.

Speaking of old and Wall Street, this past Saturday we had the Berkshire Hathaway Annual Meeting, albeit a different type without the usual tens of thousands of shareholders from around the world present.

Warren Buffet is considered one of the most successful investors in the world and his firm, Berkshire Hathaway, is the sixth-most valuable U.S. company and likely its most diversified. The conglomerate’s wholly-owned subsidiaries range from the BNSF railroad to Geico insurance, Dairy Queen, Brooks Sports, Fruit of the Loom, and a collection of utility companies. It also owns a sizable equity portfolio that includes large minority stakes in Apple, Coca-Cola, American Express, airlines such as United Continental Holdings, and Delta Air Lines, and banks including Wells Fargo and Bank of America.

One of Warren Buffet’s favorite sayings is: “Be fearful when others are greedy and greedy when others are fearful” yet during the financial turmoil of the first quarter it appears they were more fearful as they bought a relatively small amount of their own stock and equities broadly, plus sold their entire portfolio of airline holdings. With $137.2 billion in cash and equivalents is this something our listeners should pay closer attention to?

Yes, I was quite surprised to learn Berkshire Hathaway was a net seller of equities in 1Q20 and clearly wondered whether Warren Buffett was backing away from the stockmarket as finding it insufficiently attractive to appeal to his value-oriented investment approach.

Then with Berkshire Hathaway’s considerable insurance operations, perhaps it is best not to be a long-term investor when confronted by the need to fund immediate insurance policy payouts. Also, in its non-insurance activities, it is important to note that Berkshire Hathaway was not only invested in four major U.S. airlines, but also stepped up its exposure to the aerospace manufacturing sector through its 2016 $37.2bn acquisition of Precision Castparts Corp. So, not surprised if the aerospace sector’s hard landing from COVID proved to be a distraction.

Meanwhile, Fed Chair Powell has ensured credit markets remain open and liquid as evidenced by last week’s $25bn Boeing debt raise (could have taken down $70bn based on indicated interest). In so doing, the Fed has perhaps denied Buffett the opportunity to do his favorite convertible preferred deals as he did in 2008 with GE and Goldman Sachs.

Buffett may invariably strike opportunity in this market, but perhaps he is more likely biding his time to see how long the recession lasts and what floats to the surface in the meantime. It is said good things come to those who wait, so perhaps it is best we look to the wisdom in Buffett’s patience and pick our spots as well.

Let’s move away from a Macro discussion of the markets and look at a theme that has been “taking shape” for quite some time but with the COVID-19 crisis has become an everyday concern for every business – Cyber Security.

I read recently that according to the Bureau of Labor Statistics, only 29% of Americans were able to work from home before the COVID-19 era but that 99% percent of workers would choose to work remotely if they could, for at least part of the time and for the rest of their careers!!

Today, when most employees are left with no other choice but to work from home, they, as well as their employers are starting to notice the multiple complications that remote work involves. While some businesses have a good enough cyber and network security system in place, many are not aware of the risks involved in connecting remotely.

According to a Senior Analyst from the Global Cyber Center “Organizations of all kinds are facing an uptick in email-based threats, endpoint-security gaps and other problems as a result of the sudden switch to a fully remote workforce. It’s now more important than ever to consider both the security practitioner as well as ethical-hacker perspectives in order to stay secure, that’s what this is all about.”

As someone who has done a significant amount of work in the Technology field and is very familiar with Cyber Security from your work on Blockchain. I know our listeners would be interested in your thoughts as well as any investment themes around the topic of Cyber Security.

Rick, you are spot on in saying that the sudden COVID-necessitated shift to the distributed “work from home” labor footprint will expose the cybersecurity vulnerabilities of a wide range of organizations and elevate the priority of establishing and maintaining operational security. What was something that could be addressed over time before COVID has become something that must be put in place with far greater urgency.

The threat actors in cybersecurity are highly organized. According to the 2019 Verizon Data Breach Investigations Report (DBIR), organized criminal groups (39%) and nation-states (23%) were associated with 62% of data breaches. Small businesses were the leading target (43%) followed by public sector entities (16%) and healthcare organizations (15%). More often than not it is through small firms within an extended enterprise supply chain that larger firms become vulnerable.

What is interesting to note, but fully understandable as the internet has become part of our daily lives, is that while the number of websites used by individuals has grown to well over 100, the number of passwords an individual will use is likely to be 5 or fewer. The rise in the use of social media has been a major driver in the cybersecurity attacks. Combine the impact of COVID in putting more manhours of activity online and it is easy to see the problems this creates.

In terms of enhancing cybersecurity, moves to two-factor authentication may prove helpful, but what is more likely require is a more dynamic means to store and manage credentials. For investors looking to invest, there are two ETFs to consider – The Trust NASDAQ Cybersecurity ETF (CIBR) and the ETFMG Prime Cyber Security ETF (HACK).

David, I am going to ask you to get into your “way back” machine, maybe a DeLorean with a flux capacitor, and go back to your days as an Auto Analyst. There is no doubt that the

COVID-19 Pandemic is producing economic, political, and social disruptions not seen in decades, and major industries, from finance to airlines, have already felt the impact.

But the pandemic’s effect on automakers has been massive. After the virus appeared in China, auto sales there fell -80%.

Globally, the industry has canceled large events—the Geneva Motor Show and New York’s equivalent for fear of spreading the virus. European carmakers began temporary factory closures amid health concerns for their employees, falling demand, and severe disruptions to manufacturing supply chains, which often include China. And now the US industry is shuttered as well.

Like many things, the COVID-19 Pandemic will cause lasting changes. The Auto industry and the traditional gas-powered vehicle have long been “under assault” with the most visible, not to mention vocal, foe Tesla, but what do you see for the Automotive industry? Are we looking at another “Cash for Clunkers” program?

Rick, speaking of flux capacitors, in considering our future it’s important to know that where we’re going we don’t need roads as transportation and delivery services are considering alternate means such as drones and in time automated vehicles. However, getting there is going to take time so in the meanwhile it is very likely government programs aimed at stimulating the economy by encouraging consumers to trade in older vehicles for new models will prove to be essential.

Based on the April 2020 monthly auto sales data released Friday 5/1, the annualized sales pace was 8.6mm vehicles, down -48% from the April 2019 annualized sales rate of 16.4mm vehicles. Due to COVID, industry sales forecasts for 2020 have been cut. J.D. Power expects U.S. auto sales of 12.6-14.5mm vehicles, down on average -20% from an estimated 16.8mm prior to the pandemic.

In terms of a “cash for clunkers” program, in 2009 there was a $3bn package that stimulated about $14bn of purchases. Morgan Stanley estimates that the 2020 downturn may see a $10bn package that drives $50bn of purchases. In magnitude and timing, this would increase the annualized selling rate by 4mm over a 6-month period from 4Q20 to 1Q21.

Since 2020 is an election year, it is good to know the importance of the U.S. auto industry to manufacturing and employment, particularly in Michigan, Ohio, Indiana, Illinois, Texas, Kentucky, Tennessee, Mississippi and Alabama. This program would serve to keep factories in operation and directly support 3-4mm jobs, indirectly 15mm jobs, not to mention providing sales tax revenue across the country.

Note that without some industry policy measure the auto industry loses 2-3 years due to the COVID economic shock. This in a business that is important for employment and national security and significant for helping to determine how to address challenges such as electric vehicle infrastructure, battery manufacturing, renewable energy, high-speed rail, vertical-takeoff-and-landing aircraft, autonomous cars.

David as we wrap another episode this week, I think our listeners would be interested to hear your perspective on something many of us have been talking about and is perhaps the most prevalent question on Wall Street – have we been set up for a significant additional sell-off because if history is any guide, when the stock-market slips into a bear market, typically defined by a decline of at least -20% from a recent peak, it tends to return to that low more often than not, so in your opinion will market re-test the bear-market lows put in on March 23 and what portfolio or asset allocation changes should clients be considering?

As mentioned earlier, with The Fed and 1Q20 corporate earnings season out of the way investors’ attention will be drawn to the challenges faced as the global economy comes out of its first round of COVID lockdown along with news of advances in developing COVID tests and possible vaccines.

Complicating matters here is the possibility of renewed tension between the U.S. and China that may serve to slow the pace of recovery. The questions as to how COVID began and spread are legitimate so investigation will be needed, but with lesser priority than the need for a globally coordinated effort to develop a COVID vaccine.

Meanwhile, as mentioned earlier, the need for further fiscal stimulus is clear and efforts to move it forward will be needed to reassure the financial markets. However, as we wait for money and drugs to arrive, it is useful to see how countries around the world are performing on the road past lockdown.

In our previous discussions we have cited real-time traffic data from TomTom as an alternative data source. Over the weekend, data from both Europe and China show it is possible for countries to get to something like a “new normal” where citizens go to work, industrial production starts to increase again, and even weekend leisure travel returns although there are face masks, physical distancing and other COVID containment measures. As the U.S. starts down the road past lockdown, it is important to know that other countries have taken this journey and are doing it relatively safely.

With the data from other regions that are advanced relative to coming out of COVID lockdown being on balance positive it is difficult to call for a retest of the 3/23/20 stock market lows. Granted the path of recovery is on our view “W-shaped,” but we expect markets will grind higher over the course of 2020 barring the outbreak of renewed trade tensions and unforeseen COVID developments.

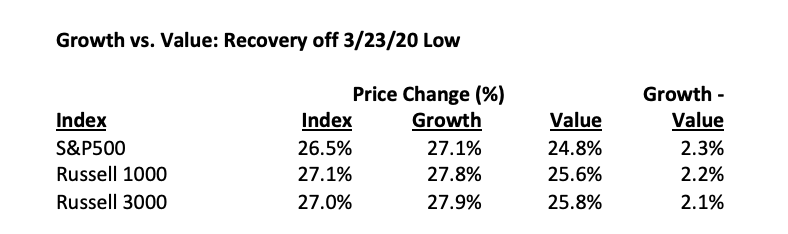

We are staying with an emphasis on large cap equities over small cap equities as we expect the big will get bigger while smaller companies will be resource constrained, something the continued elevation of high-yield bond spreads over Treasuries bears out. Similarly, we are staying with Growth over Value and expect its continued stock market leadership off the March 2020 lows as shown in the table below:

Comments are closed.