Hello and Welcome to another episode of “A Brighter Future” Laidlaw & Co’s Podcast Series. I’m Rick Calhoun CEO of Laidlaw Wealth Management and I am fortunate again to be joined by David Garrity, Chief Market Strategist for Laidlaw & Co.

Good Morning David – I trust you had a nice weekend although you needed your bar b que more for warmth than cooking. Snow in May, very odd.

Rick, not exactly the time of year for a polar vortex, but then we live in interesting times. Nevertheless, the outdoor grill was manned and ready for the Mother’s Day cookout, thank you for asking.

Odd is also a good way to characterize the markets this past week. We had bad economic data and mediocre earnings —and the stock market just kept going higher. The Dow Jones Industrial Average rose 608 points, or +2.6%, to close at 24,331. The S&P 500 index rose +3.5%, to 2,930. The Nasdaq Composite beat both its peers, rising +6% to close at 9,121, cracking the 9,000 barrier again. The Nasdaq, amazingly, is up on the year, having tacked on almost 2,500 points, or +38%, from the March lows. Not bad, considering the damage that Covid-19 has wrought on the economy. David, what’s your take on what’s going on?

Rick, there is a saying on Wall Street that you go with what is working. This is the primary insight behind the “momentum” style of investing which draws on the first law of Newtonian physics, namely that an object remains in motion unless acted upon by a force. As we know, the COVID-19 Coronavirus (COVID) pandemic has been met with a record level of fiscal & monetary stimulus which while it has not prevented a record level of unemployment as indicated by the April 2020 Employment Report released on Friday 5/8 it has nevertheless served to provide the liquidity necessary to propel stock prices as measured by the S&P 500 index to a +31% recovery from the 3/23/20 low.

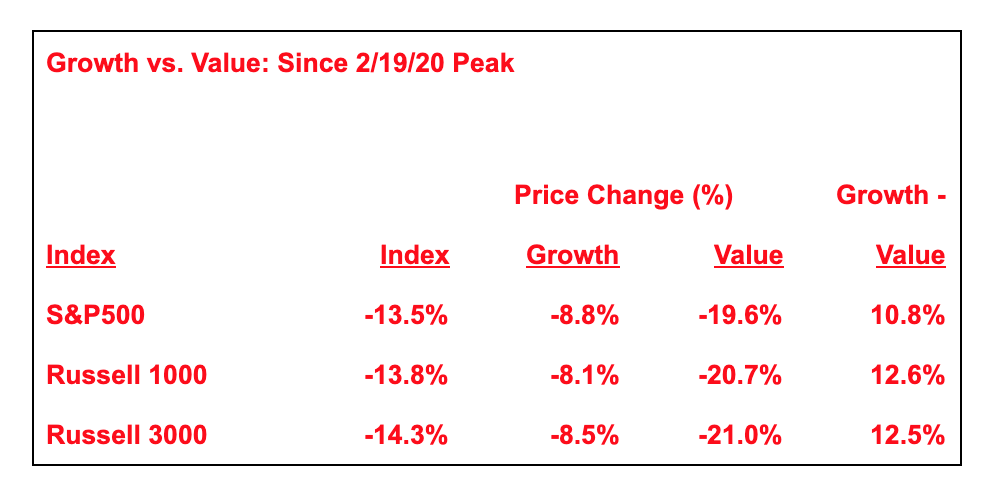

Within the stock market, growth stocks have led the recovery with a +33% gain while value stocks have posted a more modest +27% rise. This is not a function of growth performing worse than value in the S&P 500’s -34% sell-off from the 2/19/20 peak in which growth declined -31% as value plummeted -37%. With the S&P500 now off -13% its peak, investors should note that growth is down only -9% while value is still -20% down. Put it this way, if investors were long growth and short value from the peak to now, they would be +11% ahead. So, clearly growth is working in both down and up markets as shown in the table below.

The reasons supporting growth’s outperformance are relatively clear in that the shift to the COVID work-from-home (WFH) economy has made our society increasingly dependent on the technology companies who comprise a significant proportion of the growth stock index. The tech sector’s recent 1Q20 results have demonstrated continued revenue and profit growth in the face of a shrinking economy. With the likelihood that the WFH economy will persist as the return to the office will be gradual and likely not to return to pre-COVID levels, we have witnessed what perhaps should be considered an enduring repricing of the tech sector.

Bottom line, the pace of recovery is clearly uncertain and I expect that for the stock market to continue its recovery from the 3/23/20 low that further fiscal and monetary relief will be necessary. To that end, it will be critical to investors to see how Congress performs in this regard since with the upcoming general election in November 2020 the window of opportunity may be limited as campaigns get underway over the summer. Hopefully the politicians will understand that an employed constituent is a likely supporter and take the necessary actions. Meanwhile, although it has not re-covened, the U.S. House of Representatives is expected to hold votes as early as this week on a massive economic aid package for state and local governments.

David, let’s unpack the markets a little bit and talk about an area where I know you focus a lot of research – Technology. You were recently on Bloomberg Radio talking about names like GOOGL, AAPL, AMZN etc. and a few moments ago we referenced the move the NASDAQ has made off the March 23rd low but something that has become a bit distressing is the concentration of capital in what are being called “The Big 5” – GOOGL, MSFT, AAPL, AMZN & FB.

While the Nasdaq is now positive for the year, roughly 75% of the stocks in the index are down. But the Nasdaq, like the S&P 500, is weighted by market capitalization, and larger companies count for more. As of Friday’s close, the top 10 stocks, which include tech names like AAPL, AMZN, and MSFT, account for about 44% of all the value in the 2,700-stock index and those stocks aren’t cheap. On average, they trade for about 47x estimated 2020 earnings.

While the outsize weighting of major tech names fueled the Nasdaq’s bounce-back, should investors be worried?

As we have discussed previously, the present is an economic environment where the strong can rapidly become much bigger while the weak will be killed and eaten. Companies such as the “Big 5” have not only the resources needed to survive, but to thrive during COVID. Put more formally, Rick, last week noted value investor Clifford Asness published a piece defending value investing titled “Is (Systematic) Value Investing Dead.” In his analysis, “investors are simply paying way more than usual for the stocks they love versus the ones they hate (and measured using our most realistic implementation this is the clear maximum they’ve ever paid) and doing it in a highly diversified way up and down the cross section of stocks.”

The piece covers 50 years of stock market history going back to 1965 in its analysis, an impressive span of time that lends Asness’ conclusion substantial weight. However, it is interesting to note that in 1965 Gordon Moore published a paper with an insight that became known as “Moore’s Law,” which accurately predicted that computing speed/dollar would double every 2 years or so.

It is good for investors to consider that this growth in computational productivity has supported the difference we are seeing in today’s market as there is a clearly evident divide between those companies that leverage Moore’s Law and the companies that are being disrupted by it.

The period since 1965 has seen change unfold at an accelerating pace and perhaps the post-COVID WFH economy should be considered a tipping point. All I can tell you is that value investors need to be aware of how the underpinnings of our economy are shifting in making appraisals of value and allocations of capital. Otherwise, they risk coming up a dime or more short. Bottom line, if investors want more, they better get Moore.

David, let’s move to something that many veteran market watchers paid close attention to, but I don’t think the average investor did and that was when late last week, federal-funds futures began to indicate that the Federal Reserve’s key policy interest rate would fall below 0% by late this year.

While negative interest rates have been imposed by other central banks, notably the European Central Bank and the Bank of Japan, Fed officials have indicated on several occasions that they don’t favor a similar policy. While it’s still possible that we could see negative yields on U.S. Treasuries, the yield on the 2 year turning negative isn’t the same thing as the Fed “going negative”

So let me ask this as a two part question David:

First, I have read that “negative rates” is a term that’s used to describe a phenomenon that can have different meanings, can you elaborate on that for our listeners?

Rick, negative rates generally mean that a bank will charge you a storage fee for holding your cash rather than offer interest as an incentive for saving. As such with negative interest rates holding cash balances for investment purposes is discouraged and instead cash should be used for consumption because otherwise the holder of cash in penalized. With negative rates the greatest value of cash is the present. To hold it for future periods is to receive lesser value. That is the best definition of negative rates that I have.

Second, could we see negative rates in the U.S. like we’ve seen in Europe and Japan and if so, does that sentence the U.S. economy to future slow growth like we’ve seen in Japan and the EU?

Rick, the use of negative rates as a monetary policy tool has been when deflation is a significant concern. In recessions, people and businesses tend to hold on to their cash while they wait for the economy to improve. But this behavior can weaken the economy further, as a lack of spending causes further job losses, lowers profits, and prices to drop—all of which reinforces people’s fears, giving them even more incentive to hoard. As spending slows even more, prices drop again, creating another incentive for people to wait as prices fall further.

With the U.S. unemployment rate now at 14.7% and official views that the unemployment rate may rise to 20-25% before a gradual recovery unfolds paced by COVID containment measures, the U.S. economy is clearly at risk of experiencing deflation as incomes and consumer spending contract sharply. The April Employment Report presented a statistical oddity as average hourly earnings rose. This was due to how the job losses were so overwhelmingly concentrated among lower income, service industry workers.

One important point to note here is that lower income households have a higher propensity to consume, if for no other reason than they have less savings to fall back on. As mentioned earlier, Congress needs to act to provide further fiscal relief to support incomes otherwise the U.S. economy will face a significant risk of deflation among other possible negative consequences from the COVID depression. Deflation follows in the footsteps of the demand destruction pandemics such as COVID cause.

At present the Bloomberg Global GDP Tracker is indicating a -4.8% contraction in 2020. On a global basis it is estimated that a -20% contraction of income and consumption could push 524mm people into poverty (i.e. surviving on less than US$5.50/day (roughly $2k/year)). Even assuming a -10% contraction would result in an additional 249mm people living in poverty. With the COVID depression it is important for investors to consider the possibility that poverty will become more widespread in the U.S.

I want to make a 180 degree turn here David and talk about something that has been sort of forgotten and that’s Bitcoin. It was announced last week that billionaire investor Paul Tudor Jones one of the first well-known hedge fund managers, having started Tudor Investment Corporation in 1980 at the age of 25, believes that Bitcoin, the controversial digital currency, reminds him of gold in the 1970s, and may be the best hedge against inflation in the age of coronavirus.

Paul Tudor Jones is definitely someone we should pay attention to, he made a name for himself and a lot of money for investors by correctly calling the 1987 crash. He also shorted Japanese equities a couple of years later just before that market collapsed and then most recently he made a call on gold in June of 2019 that has played out almost exactly as predicted. So, as someone who knows a great deal about Bitcoin, is he right?

Rick, while we earlier discussed the risk of deflation from demand destruction in the wake of the COVID pandemic, we have to consider that assuming the tsunami of fiscal and monetary relief works in serving to stabilize the global economy and putting it on a path towards recovery there will be a distinct possibility inflation returns.

To that end, Paul Tudor Jones co-authored a paper published last week titled “The Great Monetary Inflation” in which he notes, “in a world that craves new safe assets, there may be a growing role for Bitcoin.” Jones offers this insight in the knowledge that monetary aggregates such as M2 are growing at the fastest rate since the end of WWII when annual M2 growth peaked at almost +27%. As the Federal Reserve is primarily focused on the employment support element of its mandate, Jones notes that “any (interest rate) hiking cycle is likely to be delayed and unambitious.” Separately, Jones sees in the COVID pandemic inflationary developments as “a breakdown in global supply chains spills overs to goods prices, undoing two decades of disinflation attributable to globalization.”

Against this analytical backdrop Jones offers a roster of likely inflation hedges in which Bitcoin ranks #4 after #1 Gold, #2 The Yield Curve (long 2-year bonds, short 30-year bonds) and #3 The NASDAQ 100. No wild-eyed cryptocurrency libertarian, Jones is just a seasoned successful investor “who wants to capture the opportunity set while protecting my capital in ever-changing environments.”

For Jones, Bitcoin represents “the only large tradeable asset in the world that has a known fixed maximum supply.” In a world where currencies are being devalued through massive monetary stimulus, assets that have a relatively fixed supply such as Bitcoin and gold are effective hedges against the anticipated inflation to follow.

David, as we wrap another episode this week, I thought maybe we could look ahead a little bit. Last week Professor Jeremy Siegel from the U of PA said “we’ve seen the lows in March and we will never see those lows again” expressing optimism about the path forward for the U.S. stock market, despite a historically bad jobs report. However, it’s his final statement that I’d like to focus: “I think 2021 could be a boom year, with the liquidity that the Fed is adding it could be a really good year.”

Do you agree?

Rick, focusing on Siegel’s point relative to liquidity, I agree that the March lows are unlikely to be re-tested on the conditions that Congress acts to provide further fiscal relief and that measures to contain a second wave of COVID infection prove effective.

On the first qualification, we noted earlier that the U.S. House of Representatives will likely act this week to provide further relief, but this is no guarantee that the U.S. Senate will approve, especially as Majority Leader Senator McConnell has taken the view that states should be allowed to declare bankruptcy to restructure obligations such as public sector pensions. To our view, such a political exercise would be akin to playing a game of musical chairs on the decks of the S.S. Titanic.

As to whether COVID containment measures will prove effective, we note that infection rates in the U.S. outside of New York City have remained high. Consequently, it is possible that with at least 10 states moving to re-open without meeting CDC guidelines a spike in infection rates may occur in June.

Consequently, we are at a delicate point, but I remain cautiously optimistic that the market will continue to grind higher from here as Congress moves to provide further liquidity and COVID is contained. That said, go with what is working, go with growth.

Comments are closed.