Tech Mega-Cap 2Q20 Results Will Be Released Shortly – What Should Investors Expect & Are The Stocks Worth Considering At These Levels?

COVID is providing the Tech sector a window to pursue disruption on steroids.

For example, e-Commerce share of U.S. retail sales has grown more in the past 12 weeks than it did during the last 10 years, rising to 27% of U.S. retail sales in 2020 from 16% in 2019. Meanwhile, amidst signs COVID resurgence is underway, US households are going through their largest and quickest hardware upgrade cycle ever, first after lockdowns and now as families get ready for back to school and work in the fall. Over half (55%) of consumers expect both K-12 and college students to take at least some of their classes at home in the fall, while just over a quarter (26%) think most or all classes will take place in-person. Aggregate spending for both K-12 and college is forecast to top $100 billion for the first time, or $101.6 billion, more precisely, a gain of +25.9% compared to $80.7 billion in 2019. Bottom line, moves of this magnitude taking place in the midst of the COVID pandemic serve to underscore Tech’s immediate necessity for consumers and businesses alike. More names than just Apple, Dell and Hewlett-Packard will benefit here, so the comments coming from the managements of Alphabet, Amazon, Apple, Facebook and others on their results conference calls will be telling.

COVID has brought about a world where a decade’s worth of technology adoption has taken place in as many weeks, something that favored tech sector incumbents with the products, services and capital allowing them to fully exploit this opportunity.

From a valuation standpoint this served to bring forward out-year earnings much closer in time to the present. With the drop in interest rates attending the sudden recession and the concomitant central bank monetary intervention, the discounted value of these earnings expectations has supported the increase in tech mega-cap share prices.

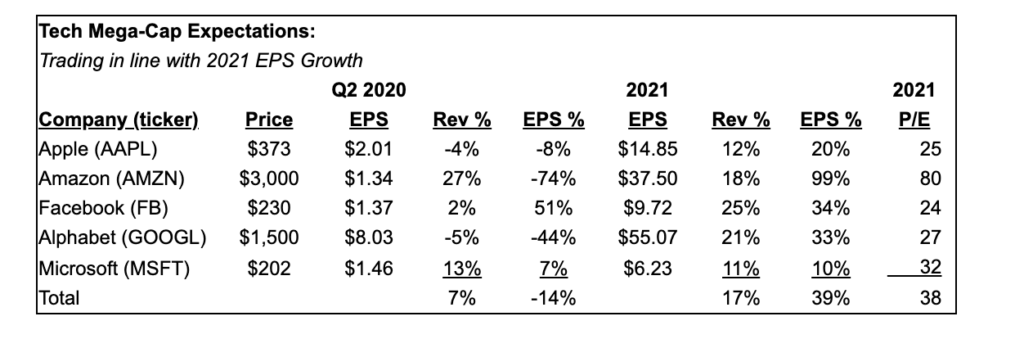

As shown in table below, the tech mega-caps are trading at 38x forecast 2021 EPS. With the 2021 EPS growth expected to be +39% on revenue growth of +17%, the implied price-to-earnings growth ratio (PEG) is roughly 1.0x. Historically, growth stocks have traded in a PEG range of 1.0-1.5x. So, by this measure of value relative to growth, tech mega-caps do not appear to be over-priced as of yet.

Separately, investors may have noticed that the U.S. Dollar has been weakening steadily against other currencies in part reflecting its weaker economic recovery on a relative basis. To the extent that the Tech sector has roughly 60% of its revenues from overseas markets, a weaker U.S. Dollar actually has a positive translation impact on the sector’s financial performance.

Tech CEOs Testify Before Congress – What Should Investors Expect?

Away from the relatively positive fundamentals for the Tech sector, today will bring testimony before Congress from leaders such as Amazon CEO Jeff Bezos in his first D.C. appearance as they are questioned on competitive practices in the sector.

With the Tech mega-cap names trading in line with their underlying EPS growth rate, we are prepared to take the risk from possible regulation in stride as the imposition of such will take time and the companies have had the opportunity to organize an effective lobbying effort to shape the form such regulation may eventually take.

Relative to each companies position, here is what defense of current business practices each company is likely to offer:

Amazon – Bezos is likely to say that Amazon is actually quite small, arguing that e-commerce makes up about only 12% of all retail sales in the United States and that Walmart sells more than his company. As noted earlier, the onset of COVID has accelerated the shift of U.S. retail sales towards e-commerce, so Amazon is likely to be seen as posing a greater competitive threat among the companies testifying. Also, despite Amazon trying to point towards the growth of 3rd party sellers off its platform, there have been additional costs levied by Amazon on the 3rd parties such that their profit margins have contracted. Separately, Amazon will have to answer as to how it is using the data gathered from its platform to develop products that compete with the 3rd parties.

Apple – CEO Tim Cook is likely to argue that Apple is not a monopoly because it controls just 15% of the global smartphone market. While this is true, it obscures the fact that the iPhone has a much higher market share in industrialized nations, including about 42% in the United States, and, in 2019, Apple said it received about 15% of the $519bn in overall commerce in the App Store. Separately, Apple will need to answer likely questions around how 3rd party apps are ranked in the App Store as it appears that either Apple apps or those of developers who pay fees to Apple are favored.

Facebook – CEO Mark Zuckerberg is likely to point to TikTok, a Chinese-backed video app, as a sign that competition in social networking is thriving, and highlight the vast digital ads marketplace to argue that Facebook has no advertising monopoly. In pointing to TikTok, Zuckerberg plays into the Trump Administration’s policies relative to China. However, the fact remains that with 2.99bn users Facebook dominates the global market with TenCent’s WeChat service in China at 1.2bn users followed by TikTok at 800mm, Snap at 238mm and Twitter at 186mm. As a result it is not surprising to see that Facebook with an estimated $74bn in 2020 digital ad revenues garner a 23% market share, trailing only Google with a 29% market share.

Google – CEO Sundar Pichai is likely to argue that Google has plenty of internet-search competition and that its high market share is because people like its products and that the company has helped drive down prices in advertising and increased choices for advertisers. As one of its highest expenses Google pays Apple fees to be the default search engine on Apple products. If its search engine were truly the most popular would such payments be required? Meanwhile, although Google contends that it has helped to lower the prices charged for digital advertising by 40% there have been independent studies done (e.g. the U.K. Competition & Markets Authority) that indicate Google prices were +30%-40% higher than those for Microsoft’s Bing search ads, when comparing like-for-like terms on both desktop and mobile.

Away From Tech Mega-Caps, Are There Other Companies In The Sector To Consider?

2020 is an election year and elections have over time only become more expensive. For example, back in June 2019, Group M, a prominent ad agency, estimated spending for political ads in 2020 will reach $10 billion, an increase of +59% from the 2016 election year when an estimated $6.3 billion was spent.

With the onset of COVID, the level of digital engagement by the U.S. population has increased substantially, something seen in the 1Q20 results for Alphabet, Facebook, Snap and others providers.

The net result is the distinct possibility that digital is set to gain a substantial reallocation of the 2020 election ad budget, something that will serve to boost 2H20 results for these companies as well as Verizon (parent of Yahoo! and AOL), Comcast and AT&T.

Among the constituencies likely to prove critical to the 2020 election outcome, Millennials will be an area of focus. In this regard, Snap is of particular interest as evidenced by the following:

“Snapchat is a hot battleground in the 2020 election. Meme-like videos have helped Trump nearly triple his following to more than 1.5 million in about 8 months, far exceeding Joe Biden’s audience. But Biden is wising up as he is giving interviews on Snapchat’s political news show, Good Luck America. Millennial and Gen-Z voters make up 35% of the U.S. electorate, and Snap says the app reaches 75% of them a day.”

Bottom line: Investors should consider holding a basket of stocks leveraged to the rise in 2020 election cycle spending which should support, if not improve, their relative performance over the next 3+ months.

Comments are closed.