Mega-cap tech stocks have been leading the U.S. market higher and David Garrity, chief market strategist, Laidlaw Wealth Management, says they’re not over-priced, at least not yet. He says the accelerated growth that companies are enjoying make the sector a defensive portfolio holding. We also dig into the latest results from Microsoft, which Garrity says remains an attractive investment at current levels.

1) Re: Microsoft’s results …whether this is a stock worth buying into at current levels given the results and the big run higher it has had this year.

MSFT overall results (Revs $38bn +13% year/year (consensus $36.5bn), EPS $1.46 +7% y/y (consensus $1.36)) were good, but the fly in the ointment is that the sales growth (+47% y/y) and margin expansion (+100bp) in its Azure cloud computing service was less than expectations. Our view is that MSFT is positioned to continue to benefit from the transition globally to a more distributed workforce and that with a new Xbox gaming platform set for release this fall the shares remain attractive.

2) Do Amazon, Facebook, Apple, Alphabet still represent value?

COVID has brought about a world where a decade’s worth of technology adoption has taken place in as many weeks, something that favored tech sector incumbents with the products, services and capital allowing them to fully exploit this opportunity.

From a valuation standpoint this served to bring forward out-year earnings much closer in time to the present. With the drop in interest rates attending the sudden recession and the concomitant central bank monetary intervention, the discounted value of these earnings expectations has supported the increase in tech mega-cap share prices.

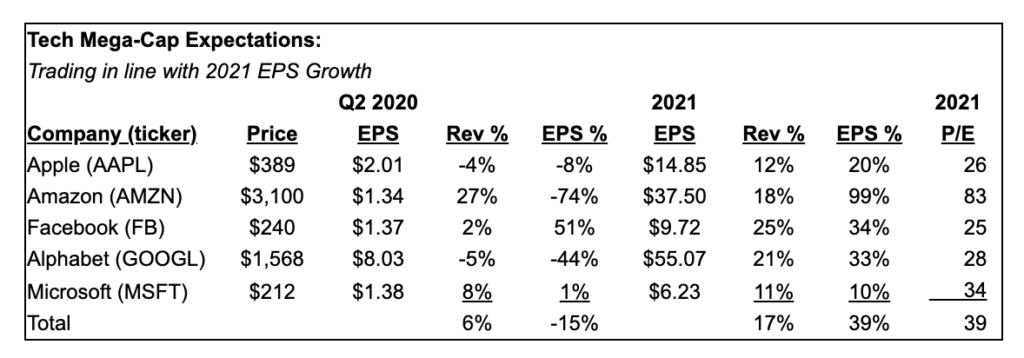

As shown in table below, the tech mega-caps are trading at 39x forecast 2021 EPS. With the 2021 EPS growth expected to be +39% on revenue growth of +17%, the implied price-to-earnings growth ratio (PEG) is roughly 1.0x. Historically, growth stocks have traded in a PEG range of 1.0-1.5x. So, by this measure of value relative to growth, tech mega-caps do not appear to be over-priced as of yet.

3) Signs of money rotating out of tech…or will it remain a sector to be in?

With economic growth prospects uncertain and clearly dependent on the continuation of substantive and substantial fiscal and monetary relief efforts to offset the negative impact of COVID the fact that tech sector is seeing accelerated growth makes it interestingly enough a defensive portfolio holding.

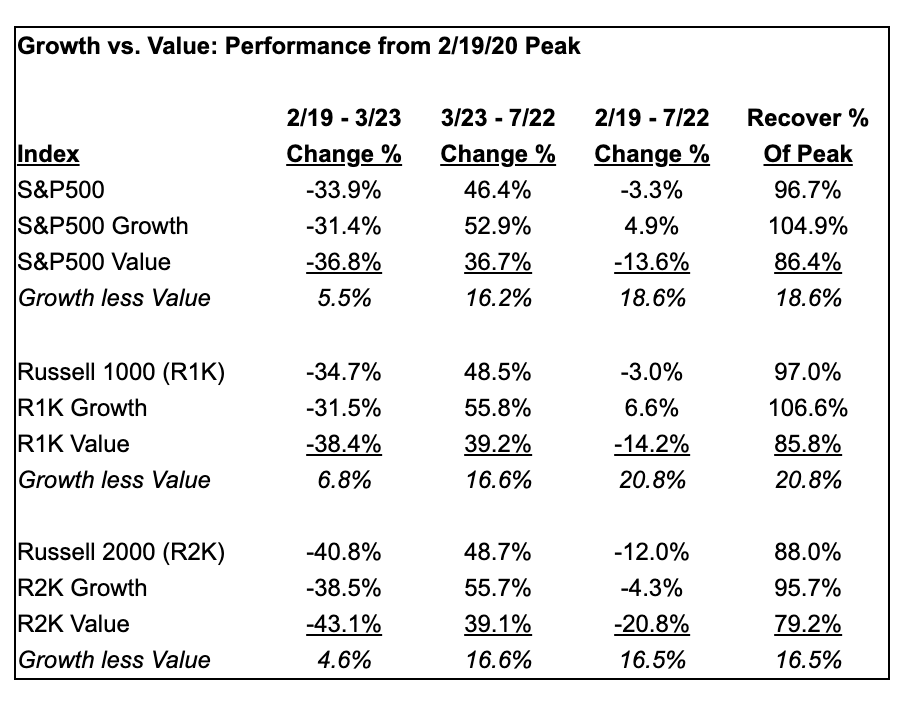

As shown in the table below, Growth has been massively outperforming Value from the 2/19/20 high in the S&P 500 index. While Value has seen brief periods of outperformance as hopes grew around the possibility of economies reopening with COVID being contained, it is Growth that should be the core holding until such time as a COVID vaccine is found and successfully commercialized.

4) Outside the handful of giants in tech that have led the market…where else in technology should investors seek opportunity? Have a couple of favored names?

2020 is an election year and elections have over time only become more expensive. For example, back in June 2019, Group M, a prominent ad agency, estimated spending for political ads in 2020 will reach $10 billion, an increase of +59% from the 2016 election year when an estimated $6.3 billion was spent.

With the onset of COVID, the level of digital engagement by the U.S. population has increased substantially, something seen in the 1Q20 results for Alphabet, Facebook, Snap and others providers.

The net result is the distinct possibility that digital is set to gain a substantial reallocation of the 2020 election ad budget, something that will serve to boost 2H20 results for these companies as well as Verizon (parent of Yahoo! and AOL), Comcast and AT&T.

Among the constituencies likely to prove critical to the 2020 election outcome, Millennials will be an area of focus. In this regard, Snap is of particular interest as evidenced by the following:

“Snapchat is a hot battleground in the 2020 election. Meme-like videos have helped Trump nearly triple his following to more than 1.5 million in about 8 months, far exceeding Joe Biden’s audience. But Biden is wising up as he is giving interviews on Snapchat’s political news show, Good Luck America. Millennial and Gen-Z voters make up 35% of the U.S. electorate, and Snap says the app reaches 75% of them a day.”

Bottom line: Investors should consider holding a basket of stocks leveraged to the rise in 2020 election cycle spending which should support, if not improve, their relative performance over the next 3+ months.

5) U.S. equity market overall…much upside left between now and the end of the year? And what is the greatest threat to continued gains in the equity market?

The stock market is discounting 2021 earnings growth that is in line with previous economic recovery cycles. Meanwhile, the Fed is clearly indicating that further monetary relief will be made available to counteract the economic fallout that might attend further COVID outbreaks. The market as a liquidity-driven flywheel is set to show further gains and as such investors should anticipate appreciation.

We note that firms such as Goldman Sachs have withdrawn lower price targets (e.g. 2,400) for the S&P 500 index as it has broken through the technically significant 3,000 level. Looking back to when the Laidlaw Five 2020 Outlook was published in December 2019, we set a 3,420 price target for the S&P 500 index. Off the 2021 estimate of $154/share, the implied P/E valuation of 22.2x is high but in our view supported by what will be an accommodative monetary policy. That said, there is a potential +4.4% gain ahead to realize the Laidlaw Five 2020 Target.

6) What has the greatest chance of throw the markets off the rails?

The brinksmanship in the U.S. Senate around the next COVID fiscal relief package has the potential to unnerve the markets. Away from that the possibility of open military conflict in The South China Sea could certainly set the markets into a correction. Ultimately, however, it is all the “unknown unknowns” around COVID that keep investors up at nights trying to determine when it is that economic recovery will be able to unfold unimpeded by repeated outbreaks.

Comments are closed.