Synopsis: “A Brighter Future”, Episode 17

In this episode Richard Calhoun, CEO of Laidlaw Wealth Management, recaps the markets and discusses the investment outlook with Laidlaw & Company Chief Market strategist, David Garrity.

The topics discussed in this episode are macro level issues such as how stock market volatility signals need for further fiscal & monetary relief, Fed Chair Powell’s Humphrey-Hawkins testimony to Congress, prospects for the new bull market, how COVID crisis recovery may involve infrastructure spending and whether globalization has ended.

Please tune in for more timely insights.

TRANSCRIPT:

Hello and welcome to another episode of “A Brighter Future”, Laidlaw & Co’s Podcast Series. I’m Rick Calhoun CEO of Laidlaw Wealth Management and I am fortunate again to be joined by David Garrity, Chief Market Strategist for Laidlaw & Co.

David, great to be with you again after another eventful and volatile week in the markets. So let’s get into it.

Last week, we saw stocks log their worst weekly declines since March as fears of a second wave of infections and doubts about a speedy economic recovery dampened investor sentiment. The Federal Reserve indicated that rates are likely to remain near zero until 2022 and issued a cautious economic outlook. The Fed’s cautious tone, in combination with news of an acceleration in new infections and hospitalizations in certain states as well as concerns about the speed of the rebound in stocks, triggered some profit-taking. So, was it just that, David, profit-taking after a great run from the lows or should we be worried?

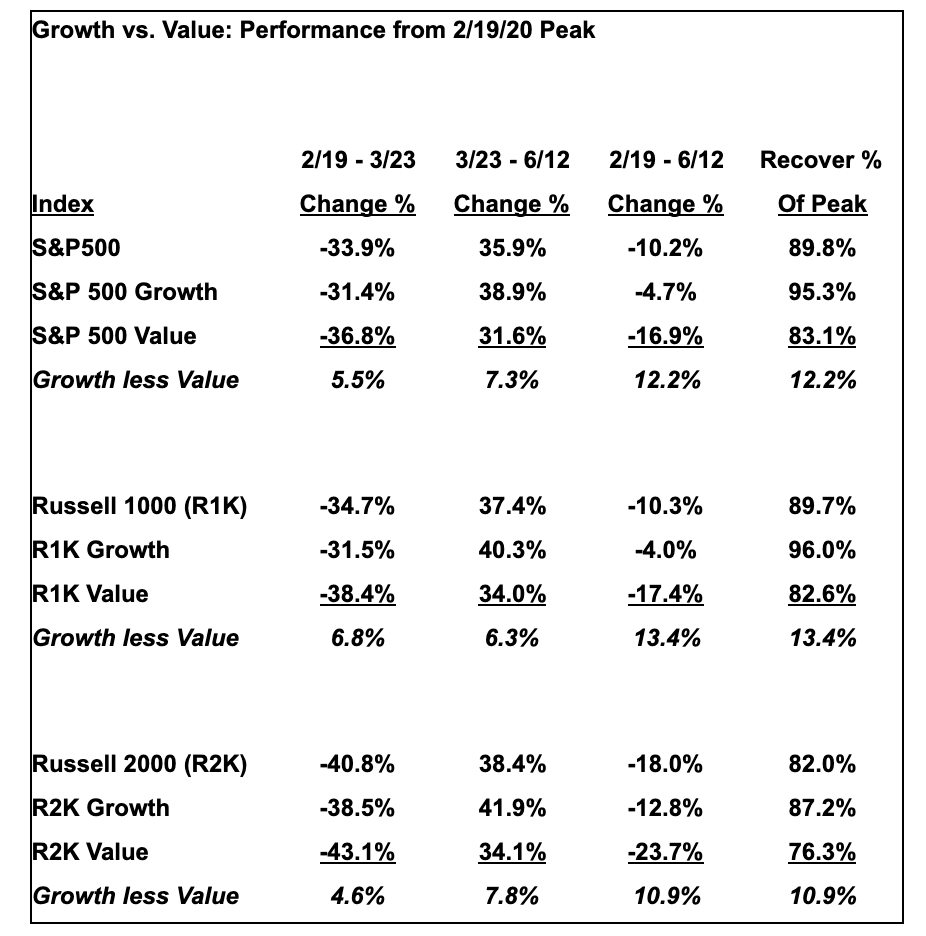

Rick, Despite last Thursday’s violent -5.9% sell-off in underwhelmed reaction to Fed Chair Jay Powell’s press conference on Wednesday afternoon, the S&P 500 index at 3,041.31 closed the week and is still up +35.9% from the March 23rd low, although with a decided tilt towards Growth (ticker IVW $200.78, +39.9% vs. 3/23/20) over Value (ticker IVE $109.19, +31.6%) as the broader global macroeconomy remains plagued by the COVID-19 Coronavirus (“COVID”) pandemic. This still leaves room for a further -5% correction from current levels to trade in the 2,800-3,000 range considered “fair value” for the S&P 500.

Apart from profit-taking spurred by Powell’s tentative remarks, the news of renewed COVID outbreaks globally along with rising civic unrest, the fact that last week saw the return of the “-5% daily move” in the S&P 500 index prompts a quick review of the significance of this kind of volatility.

Since it was formed in 1957 the S&P 500 index has had only 27 days when it has fallen by -5% or worse. As the average daily change in the S&P 500 index is less than 1%, this indicates that a move of -5% or worse in a single day lies more than 5 standard deviations (“sigma”) from the average. Based on the principles of probability, such a move should only occur once every few thousand years or so, not something that can or should be attributed to normal profit-taking.

Over the span of the S&P 500 index’s history, the greatest cluster of “-5% daily moves” was 12 days during the Financial Crisis & Great Recession of 2008-2009. With the Thursday 6/11/20 decline marking the 5th day of such negative volatility during the current downturn, the COVID crisis is now ranked #2 in terms of equity market volatility. So, what does this all mean?

To our view, such volatility is a clear and unequivocal signal that government fiscal and monetary policy is lagging economic reality, something that is troubling as one might expect with a general election less than 6 months from now that politicians would rather put themselves ahead of the curve than to run so disastrously behind it.

While there have been and still are hopes for a “V-shaped” recovery (e.g. see Morgan Stanley on the side of the “V-shaped” recovery, J.P. Morgan on the side of something more modest), the evidence is that until such time as consumers feel economically secure and physically safe the pace of recovery will be measured. Consequently, time for Congress to stop dithering and get on the ball in passing the next fiscal COVID relief package. As it is, with November fast approaching, their jobs are at stake.

David, not a week has gone by since the beginning of this pandemic where we have not discussed the Fed in some way. Last week, many felt that Thursday’s “sell off” was directly related to Federal Reserve Chairman Powell’s comments in his Post FOMC Press Conference. Powell essentially said: The economy is a disaster and we don’t see any signs of an imminent rebound, but the Fed will be here to do whatever it takes to support the economy until it gets better. Which to me says the “Fed Put” is in play and reminds me of your past comments of the Fed (and the trend) is your friend. What is more worrisome though, is that the FOMC and Powell made virtually zero mention of a sustainable economic rebound. What are your thoughts from a Macro perspective on how we can achieve that sustainable economic rebound?

Rick, When the COVID crisis is finally resolved, I fully expect there will be a re-make of the 1999 film “Being John Malkovich”, but this time it will be titled “Being Jay Powell” as clearly everyone is trying to get inside the mind of the Fed Chairman. Meanwhile, your guess on which actor will be cast for the leading role is as good as mine.

That said, Jay Powell this week has the opportunity to clarify his macroeconomic thoughts not only once, but twice, as part of the semi-annual Humphrey-Hawkins testimony before Congress on Tuesday 6/16 and Wednesday 6/17 in which he will explicate the Federal Reserve’s Monetary Policy Report that was submitted last Friday. So, stay tuned on this front for Jay Powell to have the chance to be more definitive in his words regarding the macroeconomic outlook.

Meanwhile, with the Federal Reserve acting to back-stop the credit markets and so helping to tighten the spreads over Treasuries for investment grade (IG) and high-yield (HY) issues, last week did see something of a reversal as spreads widened out a bit. Nevertheless, corporate bond spreads were more resilient than stocks during Thursday’s risk asset selloff. Although so far in June the S&P 500 is lower, IG spreads remain lower by 17 basis points and HY by 14 basis points as of Thursday.

What may be interesting in Jay Powell’s upcoming testimony, among other topics, is the possibility the question may be posed of whether the Fed has considered extending support to the equity market. Equities don’t have that backstop now and last Thursday was a 5-sigma down day. Bonds do have the Fed back-stop, so while spreads widened last week, fixed income price action was nowhere near as dramatic as what was seen in stocks. Just saying.

Meanwhile, for thoughts on ways in which to achieve a more sustainable economic rebound we offer some fiscal policy considerations later in the discussion in the context of considering not just recovering from COVID, but in putting in place the energy infrastructure needed to transition to a less carbon-intensive economy.

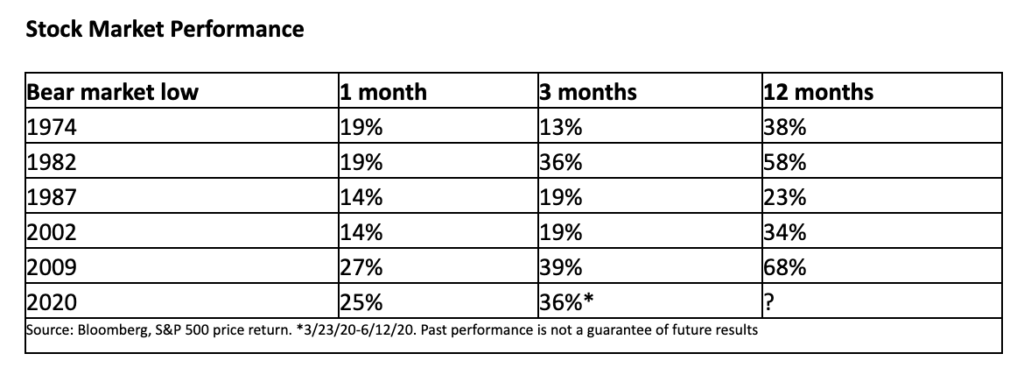

David, let’s turn our attention back to the markets. Last Thursday’s -1,800-point drop in the Dow brought back memories of the dramatic swings that were prevalent through February and March. Although the market declined -5% last week, it should not be lost that it is still +36% higher since late March and just -10% from its all-time high. I did a little homework this weekend and history shows that the initial stages of new bull markets are typically characterized by strong gains.

According to Bloomberg, in the postwar era, every instance in which the stock market rose more than +30% from a bear market low turned out to be the beginning of a new bull market. So, in your opinion, could this be the beginning of a new Bull Market?

Rick, From the standpoint of textbook definition, any -20% retrenchment, or bear market, offers the chance to bring about a new bull market. With the S&P 500 index falling -33.9% from the high on 2/19/20 to the low on 3/23/20, the first condition of having a bear market has been met. Also, as you indicate, the +35.9% return from the low does show the second condition for the consideration of a new bull market has been met.

However, given the tsunami of liquidity that has been unleashed as governments around the world have sought to mitigate the impact of the COVID pandemic, is it fair to say that this a bull market as its economic underpinnings are uncertain and the possibility that at some point the relief injected will likely be withdrawn? Such circumstances could just as easily be termed an asset bubble wherein expectations have been floated while the economy remains on the rocks.

Nevertheless, I am inclined to see that we are indeed in a new bull market, but one that will need to find its footing and as such is likely to be more of a grind higher from here than a continuation of the rocket ride from the March 2020 lows.

In this context, it may be best for investors first to build core positions in solid Growth names prior to expanding into more economically exposed Value names until the desired firmer economic footing becomes clearer.

David, there is a quote attributed to Aristotle –

“It is the mark of an educated mind to be able to entertain a thought without accepting it.”

I mention that because I recently read the headline, “Renewables surpass coal in U.S. energy generation for first time in 130 years.”

The headline, while impressive, gave the impression that renewables had made a large, unexpected, leap forward versus coal and other fossil fuels. Globally, our lives revolve around energy use, and lots of it. Fossil fuels (such as coal, oil, and natural gas) generate most of that energy today. Recent progress in renewables (like wind, solar, and hydropower) has been made, and I have no doubt that renewables are the future. But do you see fossil fuel use on the verge of collapsing?

Rick, While there was certainly a great deal of furor and speculation around the oil price crash and OPEC+ production cut pact earlier this year and the commodity’s subsequent price rebound, gasoline demand is beginning to recover in part due to people deciding to drive their own cars rather than run the risk of COVID infection by taking public transportation and, no, fossil fuel use is not collapsing. Note that in 2019 global oil consumption was running at a rate of roughly 100mm barrels per day, not something that is about to disappear overnight.

However, there is an opportunity in the COVID crisis to stimulate economic growth by public and private sector investment in climate-friendly infrastructure that will serve to create new jobs and position the global economy to address the longer run challenge of climate change.

Note that neither COVID nor greenhouse gases care much for borders, something that makes both challenges global. Furthermore, the two crises do not just resemble each other, they interact as shutting down the global economy has led to huge cuts in greenhouse-gas emissions. However, on a global basis, there is still more than 90% of the necessary decarbonization left to do to get on track for the Paris Agreement goal of a +1.5 degree Celsius increase in temperature levels.

This leaves open a significant opportunity to not only stimulate economic growth, put in place pricing and tax frameworks to promote the use of less carbon-intensive energy sources and produce the revenues necessary to pay for the fiscal stimulus employed to offset COVID. In this way, policy can be both penny-wise in the short-term and avoid being pound-foolish by not taking advantage of currently lower opportunity costs to put the global economy’s energy infrastructure on better footing climate-wise for the long term.

David, as we near the end of today’s episode I’m interested in your thoughts on the pandemics effect on Globalization.

We are now seeing that the fallout from the coronavirus pandemic has capped growing disenchantment with globalization that we have observed over the past decade. Fragile supply chains worldwide have been exposed by competition for essential medical and food supplies. Unilateral export controls have been imposed to ensure availability of goods for the local market. That has compounded the pandemic’s damaging economic effects, atop the human tragedy, adding to protectionist pressures to sustain U.S. living standards.

Recent developments follow a long “hollowing out” of manufacturing and loss of high-paying blue-collar jobs, aggravating politically sensitive income inequality in the U.S. and abroad. Even The Economist sounded globalization’s death knell in a recent cover story referring to as Slowbalization!!

David, could the pandemic’s economic and human toll bring an end to globalization?

Rick, While there was already consideration of the need to re-engineer supply chains away from following the strict rule of finding the lowest price available, something in part prompted by the U.S.-China trade war, the impact of COVID has been to accelerate the implementation of these nascent plans into action.

Companies are learning from the COVID crisis to insure themselves against supply chain disruption through steps such as having at least two suppliers of every component or raw material. Until now, logistics and supply chains may have been very fragmented and very vulnerable since the overriding goal of finding the cheapest global provider led companies to overlook the value of the provider who was just around the corner.

Yet it is not just supply chains that are being reconfigured, it is the entire social and political economy that has been underpinned by globalization. As the world reopens from COVID, activity may recover, but we cannot expect unfettered movement and free trade to return. As can be seen, COVID is politicizing travel and migration and entrenching a bias towards self-reliance. To our view, this process of turning inward will undermine the economic recovery and thereby likely promote geopolitical instability.

Consequently, it is critical for efforts to be made to reach an over-arching consensus to support an open global economy or face costs that may be greater than simply having to pay a higher price for imported products. To find a way forward from COVID, I believe it better to have agreement around resilience than a divided self-reliance. As Ben Franklin once said, “We must, indeed, all hang together or, most assuredly, we shall all hang separately.”

Comments are closed.